What is a Tariff?

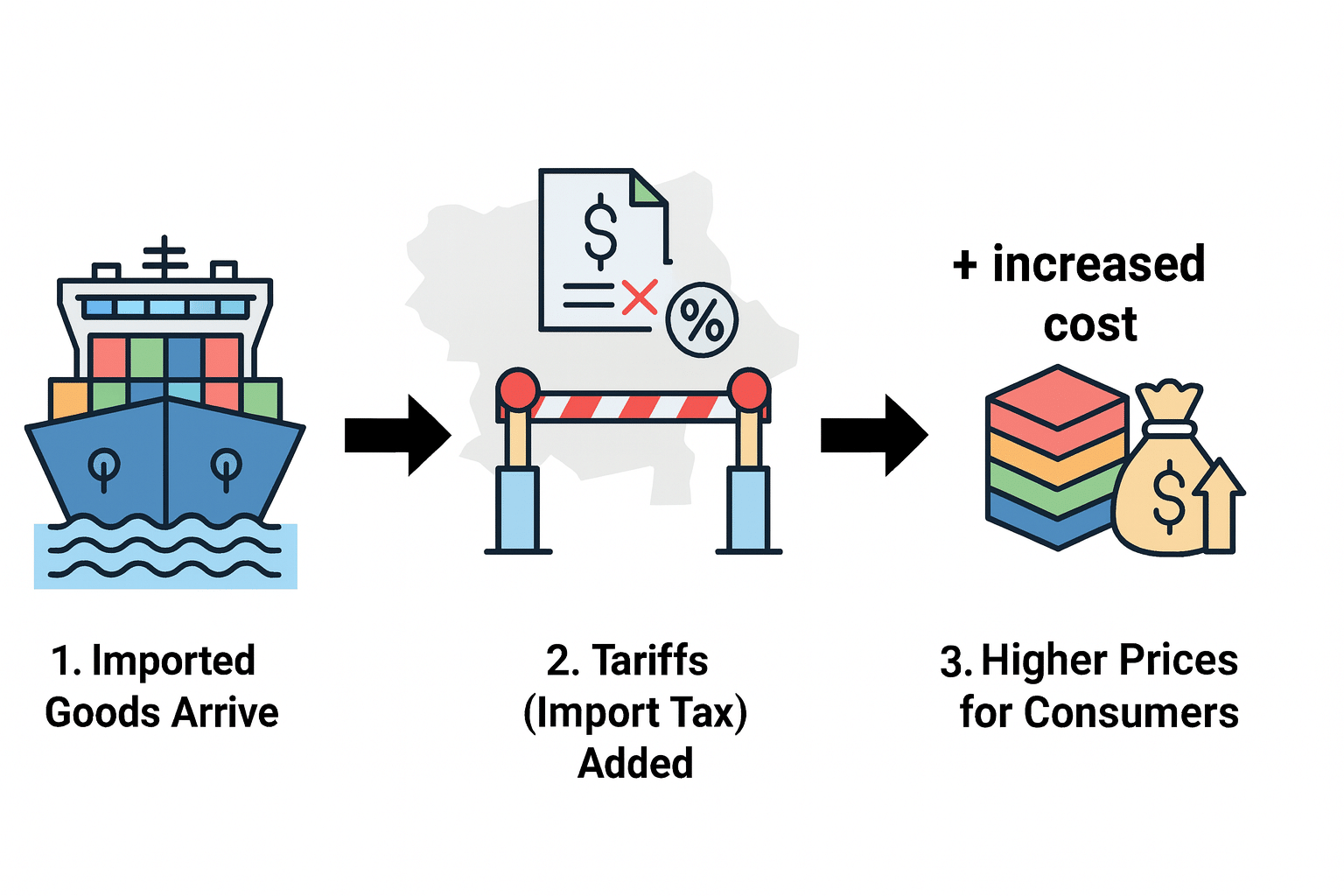

A tariff is a tax imposed by a government on goods and services imported from other countries that serves to increase the price and make imports less desirable, or at least less competitive, versus domestic goods and services. Tariffs are generally introduced as a means of restricting trade from particular countries or reducing the importation of specific types of goods and services.

For example, to discourage the purchase of Italian leather handbags, the U.S. government could introduce a tariff of 50% that drives the purchase price of those bags so high that domestic alternatives are much more affordable. The government’s hope is that the added cost will make imported goods much less desirable.

International Tariffs

By the same token, other governments can apply tariffs for the same reason. A 2010 BusinessInsider article cited China’s tariff of 105.4% on U.S. chicken as a situation gone awry and negatively impacting U.S. poultry farmers. But China’s tariff was in direct response the U.S.’s new tariff on Chinese tires, which started at 35% the first year and declined to 25% in the third as a way to shore up the U.S. tire industry.

A Pre-Income Tax Source of Funding

In addition to discouraging the purchase of imported goods, tariffs at one time were also the major source of governmental income. Until the income tax was introduced in 1913, tariff revenue comprised as much as 95% of governmental funding. Back then, typical tariffs were 20% of the product’s value.