If you are asking what is credit card tokenization, you are already thinking about one of the most important topics in modern payment security. As digital payments become the default for online stores, restaurants, retail shops, and subscription businesses, the risks tied to handling card data continue to grow. Data breaches, card-not-present fraud, and compliance failures now cost businesses billions of dollars every year.

Understanding what is credit card tokenization helps merchants see how the payment industry protects sensitive financial information without slowing down transactions. Instead of storing real credit card numbers, tokenization replaces them with secure payment tokens that hold no exploitable value. As a result, businesses can process payments confidently while protecting customers and reducing long-term security risk.

Table of Contents

- Understanding What Is Credit Card Tokenization

- How Credit Card Tokenization Works

- Security Benefits of Token-Based Payments

- Tokenization vs Encryption in Payment Security

- Why Businesses Use Credit Card Tokenization

- How Biyo POS Supports Secure Tokenized Payments

- Frequently Asked Questions

Understanding What Is Credit Card Tokenization

Before diving into technical workflows, it is important to clearly define what is credit card tokenization and why it exists. Tokenization was designed to solve a very specific and expensive problem: how to process digital payments without exposing sensitive cardholder data.

Definition of Credit Card Tokenization

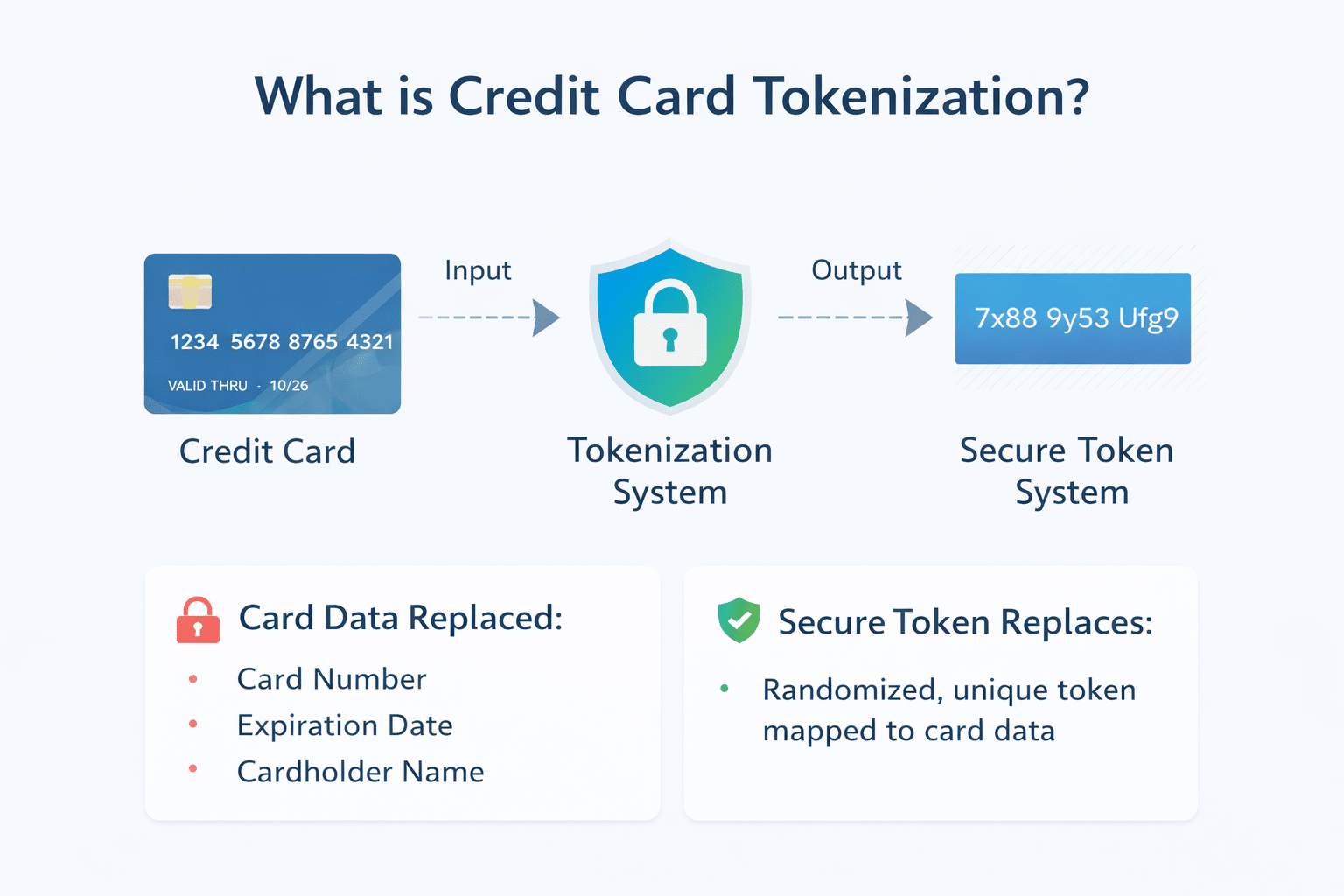

What is credit card tokenization at its core? It is a payment security technology that replaces a customer’s real credit card number with a randomly generated payment token. This token looks like a series of numbers or characters, but it has no mathematical or logical connection to the original card data. Even if someone steals the token, it cannot be reversed, decrypted, or reused outside its authorized environment.

In practical terms, tokenization allows merchants to stop storing actual card numbers in their systems. Instead, the real card data is securely stored in a payment token vault operated by a payment gateway or processor. The merchant’s database only contains tokens, which dramatically reduces exposure to sensitive data and lowers overall security risk.

This method plays a central role in cardholder data protection, secure card storage, and PCI DSS compliance. Businesses can still charge customers, issue refunds, and manage subscriptions, but they never touch the underlying financial data. That separation is what makes token-based payments so powerful in modern payment security.

Why Tokenization Was Created

Tokenization emerged as a response to the growing number of high-profile data breaches in the early days of eCommerce and digital payments. At that time, many businesses stored encrypted card numbers directly on their servers. While encryption helped, attackers quickly learned that encrypted data still had value if they could obtain the decryption keys.

Payment networks and security experts realized that the safest data is data you never store at all. Tokenization was created to remove card numbers from merchant environments entirely, rather than simply disguising them. This shift changed the economics of cybercrime by making stolen payment data far less valuable.

Today, payment tokenization is considered a foundational layer of payment security technology. It supports fraud prevention, reduces liability, and helps merchants comply with increasingly strict security regulations. Without tokenization, many modern digital payment experiences would not be possible at scale.

Where Tokenization Is Used Today

Tokenization is now used across almost every digital payment scenario. Online stores rely on it to protect card-not-present transactions, which account for a large percentage of payment fraud worldwide. Subscription businesses depend on tokenized payment processing to store customer payment methods securely for recurring billing.

In physical locations, tokenization works alongside EMV security and contactless payments. When a customer taps, inserts, or swipes a card, the transaction still results in a token being stored instead of a real card number. This approach protects transaction data after authorization and limits exposure if systems are compromised.

Mobile apps, digital wallets, and in-app purchases also depend heavily on token-based payments. Because of this wide adoption, understanding what is credit card tokenization is essential for any business that accepts digital payments or plans to scale securely.

How Credit Card Tokenization Works

Once you understand what is credit card tokenization, the next step is learning how it actually functions during a transaction. While the process happens in seconds, several critical security steps take place behind the scenes.

Step-by-Step Tokenization Process

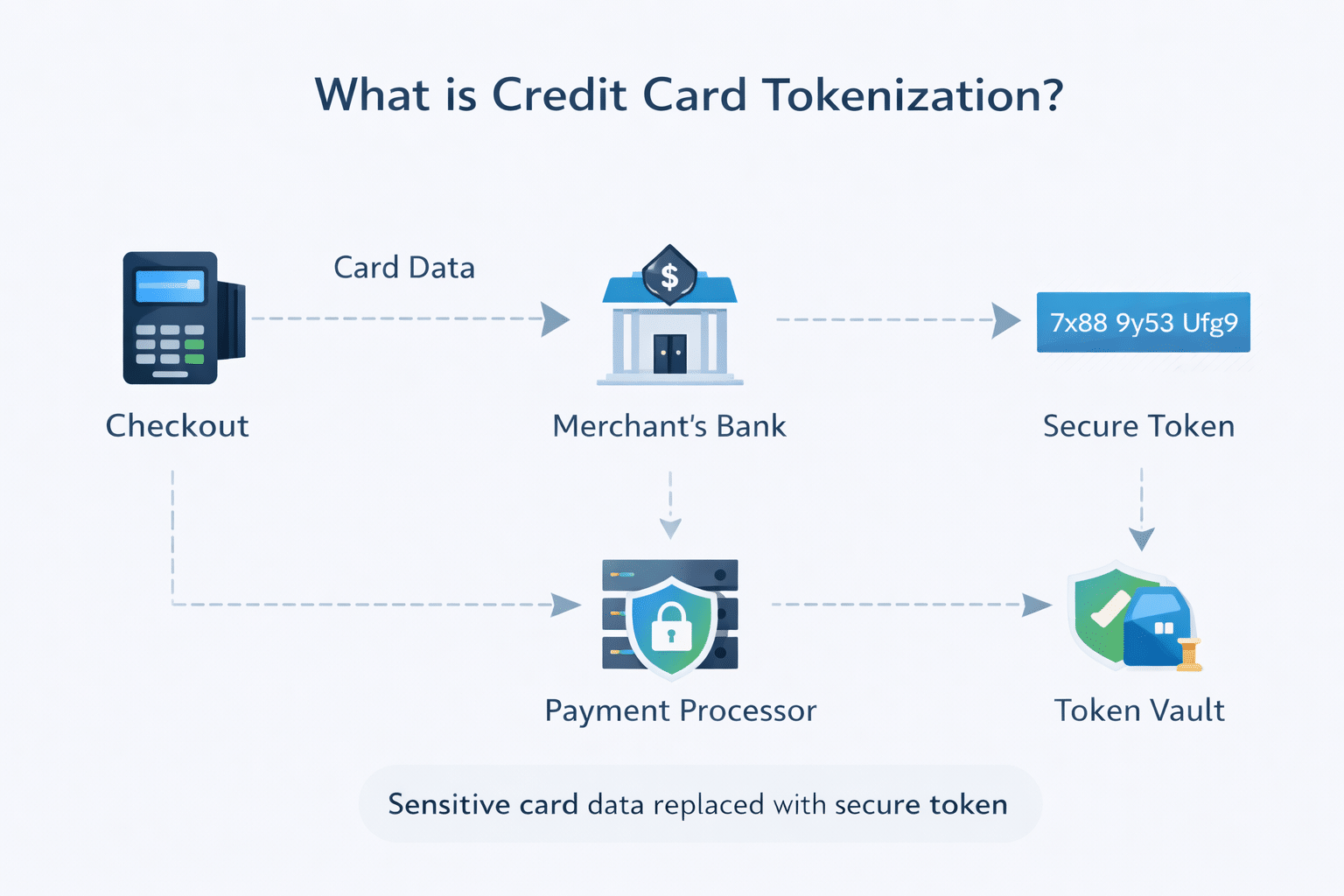

The tokenization process begins the moment a customer enters their card details at checkout, whether online or in person. That information is immediately transmitted through an encrypted connection to a secure payment gateway. At no point is the card number stored in plain text within the merchant’s system.

The payment gateway validates the card information and generates a unique payment token. This token replaces the card number in all merchant-facing systems, including POS software, order history, and customer profiles. Meanwhile, the original card data is stored securely in a payment token vault managed by the processor.

For future transactions, the merchant submits the token instead of the card number. The payment processor maps the token back to the original card data internally and completes the charge. This structure ensures encrypted transactions, strong sensitive data protection, and seamless payment experiences for customers.

Role of the Payment Token Vault

The payment token vault is the most secure component of the tokenization system. It acts as the only location where real card numbers exist, and it is protected by multiple layers of security controls. Access is tightly restricted and monitored by payment processors that specialize in financial data protection.

Because merchants never access the vault directly, attackers cannot retrieve card data even if they compromise a merchant’s network. Tokens stored in merchant systems have no standalone value. This separation dramatically reduces the impact of potential breaches and limits regulatory exposure.

From a compliance perspective, the vault also helps businesses meet PCI DSS compliance requirements. By outsourcing card data storage, merchants reduce the number of systems that fall under PCI audits, which saves time, money, and operational complexity.

Token Usage in Transactions

Payment tokens are designed to be context-specific, meaning they only work within defined environments. A token created for one merchant, device, or channel cannot be reused elsewhere. This limitation strengthens transaction safety and prevents unauthorized reuse.

When a transaction occurs, the token functions as a secure reference rather than actual payment data. The merchant submits the token, the payment gateway validates it, and the processor completes the transaction without exposing the underlying card number.

This design plays a major role in fraud prevention. Even if criminals intercept tokens, they cannot use them to make purchases elsewhere. As a result, token-based payments significantly reduce the risk of large-scale payment fraud.

Security Benefits of Token-Based Payments

One of the main reasons businesses ask what is credit card tokenization is to understand its security advantages. Tokenization offers benefits that extend far beyond basic data masking.

Reduced Risk of Data Breaches

Tokenization dramatically lowers the value of stolen data. In a breach scenario, attackers may access databases filled with tokens, but those tokens cannot be converted into usable card numbers. This reality changes the risk profile of merchant systems.

Unlike encrypted data, tokens cannot be cracked or decrypted. Without access to the payment token vault, stolen information is effectively useless. This makes tokenization one of the most effective tools for protecting credit card data.

For businesses, this reduced risk protects revenue, brand reputation, and customer trust. It also lowers the likelihood of costly breach notifications, fines, and legal action.

Improved PCI DSS Compliance

PCI DSS compliance is one of the most challenging requirements for businesses that accept credit cards. Tokenization simplifies compliance by reducing the amount of cardholder data a merchant handles directly.

When systems only store tokens, they fall outside many PCI scope requirements. This reduction leads to fewer audits, simpler documentation, and lower compliance costs. For small and mid-sized businesses, this benefit alone can be transformative.

As a result, tokenized payment processing is often recommended as a best practice for achieving long-term PCI compliance.

Enhanced Fraud Prevention

Tokenization strengthens fraud prevention by limiting how payment data can be used. Tokens are tied to specific merchants, channels, or devices, which prevents replay attacks and unauthorized transactions.

Payment gateway security tools also monitor token usage patterns in real time. Suspicious behavior, such as abnormal transaction volume or location changes, can trigger alerts or blocks.

This layered approach improves transaction safety and protects both merchants and customers from evolving fraud tactics.

Tokenization vs Encryption in Payment Security

Many people confuse encryption with tokenization when learning what is credit card tokenization. While both are essential, they solve different security problems.

Key Differences Between Tokenization and Encryption

Encryption protects data by transforming it into an unreadable format using cryptographic algorithms. If someone obtains the decryption key, they can restore the original data. This reality means encrypted card data still carries inherent risk.

Tokenization removes sensitive data entirely from merchant systems. The token has no intrinsic value and cannot be reversed without access to the secure vault. This difference makes tokenization far safer for long-term storage.

Because of this distinction, token-based payments are preferred for storing and reusing payment information.

When Encryption Is Still Used

Encryption remains critical during data transmission. Whenever card data moves between systems, encryption ensures it cannot be intercepted in transit.

Once the transaction is complete, tokenization takes over for storage and reuse. This layered approach combines the strengths of both methods.

Secure payment processing relies on encryption and tokenization working together, not competing with each other.

Why Tokenization Is Preferred for Storage

For stored payment data, tokenization offers unmatched protection. Tokens eliminate the presence of real card numbers in merchant databases.

This approach supports secure card storage for subscriptions, loyalty programs, and saved payment methods. Customers enjoy convenience without sacrificing security.

That balance is why tokenization has become the standard for modern payment systems.

Why Businesses Use Credit Card Tokenization

From startups to global enterprises, understanding what is credit card tokenization explains why adoption continues to grow.

Customer Trust and Secure Checkout

Customers expect secure checkout experiences, especially when shopping online. Tokenization helps meet those expectations by protecting sensitive data behind the scenes.

When customers trust a merchant’s payment security, they are more likely to complete purchases and return in the future. This trust directly impacts conversion rates and customer lifetime value.

Secure payment processing is no longer optional for competitive businesses.

Support for Digital and Omnichannel Payments

Businesses now accept payments across websites, mobile apps, kiosks, and physical stores. Tokenization supports all these channels using a consistent security framework.

Because tokens work across systems, merchants can unify customer payment data safely. This consistency improves reporting, analytics, and transaction safety.

Omnichannel growth depends heavily on token-based payments.

Operational Efficiency and Scalability

Tokenization reduces the operational burden of managing sensitive financial data. Teams spend less time on security concerns and more time on business growth.

As transaction volume increases, tokenized payment processing scales without increasing risk. This scalability makes tokenization ideal for growing businesses.

Security and efficiency move together when tokenization is in place.

How Biyo POS Supports Secure Tokenized Payments

Biyo POS is built with modern payment security at its core. By supporting token-based payments, Biyo POS helps merchants apply what is credit card tokenization in real-world operations.

With secure payment processing, encrypted transactions, PCI compliance support, and safe token storage, Biyo POS protects sensitive data while keeping checkout fast and reliable. Businesses can manage recurring billing, digital payments, and in-store transactions without handling real card numbers.

If you want to strengthen your payment security, schedule a call with our team or sign up to get started with Biyo POS today.

Frequently Asked Questions

What is credit card tokenization used for?

Credit card tokenization is used to protect cardholder data by replacing real card numbers with secure tokens. It supports fraud prevention, PCI compliance, and secure payment processing.

Is tokenization better than encryption?

Tokenization is better for data storage because it removes sensitive data entirely. Encryption remains important for protecting data during transmission.

Does tokenization affect payment speed?

Tokenized payment processing is designed to be fast and efficient. In many cases, it improves checkout speed for returning customers.

Can small businesses use tokenization?

Yes, most modern POS systems and payment gateways include tokenization by default. Small businesses benefit from stronger security and simpler compliance.

Is credit card tokenization required for PCI compliance?

Tokenization is not required, but it greatly simplifies PCI DSS compliance. Many businesses adopt it to reduce risk and audit scope.