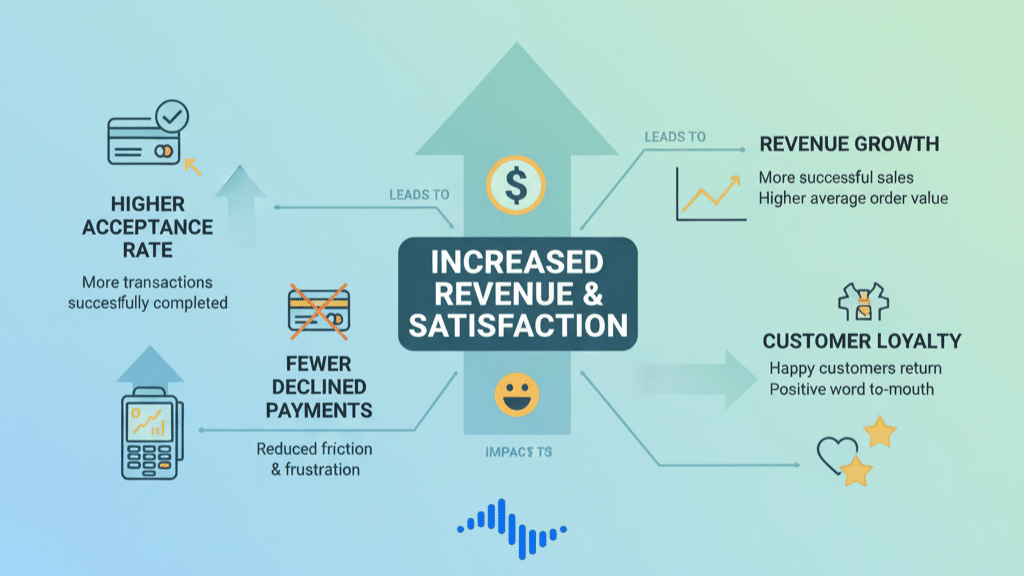

Your payment acceptance rate tells you how many payment attempts actually succeed. When this number rises, more carts convert, service lines move faster, and refunds or support tickets drop. When it falls, customers lose confidence, cash flow slows, and marketing dollars get wasted on abandoned orders.

Because payments happen at the final step of the buying journey, even small improvements can generate significant revenue gains. Businesses that monitor and optimize their payment acceptance rate often see measurable improvements in checkout conversion, customer trust, and operational efficiency.

With the right workflow, you can diagnose decline patterns, improve authorization rate, and remove the friction that prevents successful transactions. This guide explains the foundations of payment acceptance rate, the factors that influence it, and the strategies businesses use to increase transaction success across POS and online channels.

Table of Contents

- Foundations: What Payment Acceptance Rate Measures and Why It Matters

- Key Drivers: What Improves or Hurts Transaction Success

- How To Optimize: Checkout, Risk, Routing, and Retries

- Monitor and Analyze: Turning Payment Data Into Wins

- Trust and Growth: POS Integration, Reliability, and Chargebacks

- How Biyo POS Helps Improve Payment Acceptance Rate

- Frequently Asked Questions

Foundations: What Payment Acceptance Rate Measures and Why It Matters

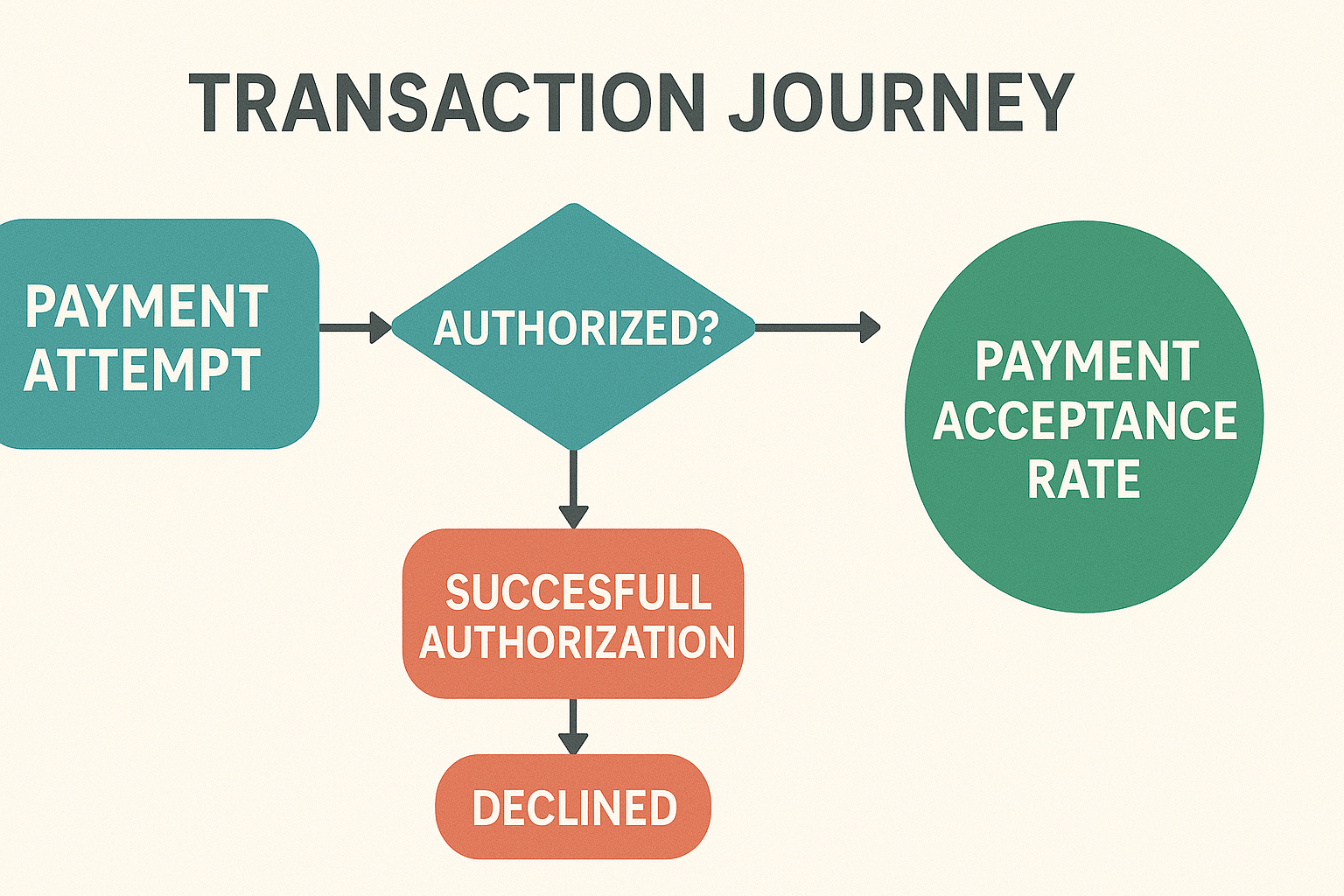

The payment acceptance rate is the share of approved payments out of all attempts. Businesses use this metric to measure transaction reliability across payment gateways, acquirers, and checkout channels.

When acceptance improves, transaction success rises and conversion rates increase. Because payments occur at the end of the purchasing funnel, even small improvements can generate large revenue gains without increasing marketing costs.

Definition, Formula, and Real-World Impact

At its simplest, the payment acceptance rate equals approved transactions divided by attempted transactions. Businesses often track this metric by device type, card brand, country, and payment channel to identify patterns affecting authorization success.

For example, if a store receives 100,000 payment attempts and 93,000 approvals, the acceptance rate is 93%. The remaining 7,000 declined transactions represent lost revenue opportunities that may be recoverable through optimization.

Even a small increase in acceptance rate can significantly impact revenue. Increasing approvals from 93% to 95% would recover 2,000 additional transactions without additional marketing spending.

How Acceptance Relates to Authorization Rate and Conversion

The authorization rate measures how often issuing banks approve payment requests. The payment acceptance rate depends heavily on this metric but also includes factors such as fraud checks, gateway performance, and checkout reliability.

Checkout friction often lowers authorization success. Long forms, multiple verification steps, or confusing error messages increase the likelihood that customers abandon the payment process.

Simplified checkout flows, mobile wallets, and tokenized card storage can reduce these issues and improve both authorization rate and acceptance rate.

Top Decline Reasons and Where They Hide

Common payment declines include insufficient funds, expired cards, incorrect billing information, or fraud screening triggers. Technical issues such as gateway latency or network outages can also prevent successful authorizations.

Often, decline patterns appear in specific segments such as certain card brands, mobile devices, or geographic regions. Segmenting payment data allows businesses to identify these patterns and apply targeted improvements.

Key Drivers: What Improves or Hurts Transaction Success

Payment acceptance depends on several factors including gateway performance, fraud prevention settings, issuer relationships, and checkout design. Improving any of these areas can increase approval rates.

Gateway Performance, Latency, and Redundancy

Fast and stable payment gateways prevent timeouts that interrupt authorization requests. Latency problems can cause transactions to fail even when the customer has sufficient funds.

Redundant infrastructure and automatic failover ensure payments continue processing even if one gateway or processor experiences an outage.

Fraud Prevention That Reduces False Declines

Fraud prevention systems must balance security with user experience. Overly strict rules may block legitimate customers, reducing the payment acceptance rate.

Combining signals such as CVV verification, AVS checks, and adaptive risk scoring helps reduce fraud while allowing genuine customers to complete transactions smoothly.

Acquirer Mix and Issuer Relationships

Different acquiring banks perform better with different card networks or geographic regions. Smart payment routing sends transactions to the acquirer most likely to approve them.

This routing strategy can increase approval rates without requiring changes to the checkout experience.

How To Optimize: Checkout, Risk, Routing, and Retries

Improving payment acceptance involves optimizing both technology and user experience.

Frictionless Checkout That Still Feels Safe

Short checkout forms reduce errors and speed up the payment process. Autofill fields, saved cards, and mobile wallets help customers complete purchases quickly.

Clear security indicators such as SSL icons and concise messaging reassure customers that the transaction is safe.

Risk Settings That Balance Safety and Sales

Businesses should regularly analyze false declines and adjust fraud rules accordingly. Strict rules should apply only to high-risk transactions while trusted customers move through checkout without unnecessary barriers.

Smart Routing and Intelligent Retries

Routing payments to the most successful acquirer for each transaction improves authorization success. Intelligent retry logic can recover soft declines by sending the payment request through an alternate path.

Monitor and Analyze: Turning Payment Data Into Wins

Monitoring payment metrics allows businesses to quickly identify issues affecting transaction success.

Metrics That Matter Every Week

Key payment metrics include acceptance rate, authorization rate, decline reason codes, gateway latency, and chargeback ratios.

Segmenting data by device, payment method, or geographic region reveals patterns that require targeted improvements.

Failure Analysis That Finds Fast Fixes

Declines can be categorized into soft and hard failures. Soft declines may succeed after retries or routing changes, while hard declines require updated card details.

Setting Targets With Industry Context

Most businesses aim for payment acceptance rates between 95% and 99%. Targets vary depending on industry, payment methods, and geographic regions.

Trust and Growth: POS Integration, Reliability, and Chargebacks

Reliable payments improve customer trust and encourage repeat purchases. When transactions consistently succeed, customers feel confident using your checkout process.

Unified POS and Online Flows

Integrating in-store POS systems with online payment platforms reduces data inconsistencies and improves payment reliability.

Operational Playbooks That Keep Payments Running

Documented response procedures allow teams to quickly address gateway outages or routing issues that affect approvals.

Reducing Chargebacks Without Hurting Conversion

Clear billing descriptors, responsive customer support, and strong evidence collection help prevent disputes and protect payment approval rates.

How Biyo POS Helps Improve Payment Acceptance Rate

Modern POS technology plays an important role in improving payment performance. With Biyo POS, businesses gain access to advanced payment routing, real-time transaction monitoring, and detailed reporting tools that help identify approval issues quickly.

Businesses can also schedule a personalized demo to see how Biyo POS integrates payment processing, analytics, and fraud protection into a single platform designed to improve payment acceptance rates.

Frequently Asked Questions

What is a good payment acceptance rate?

Most businesses aim for acceptance rates between 95% and 99%. Lower rates may indicate checkout issues, gateway problems, or overly strict fraud rules.

Why do payments fail even when customers have funds?

Declines can occur due to incorrect billing information, issuer risk checks, fraud detection triggers, or technical timeouts.

How can businesses increase payment acceptance?

Improving checkout design, enabling mobile wallets, optimizing payment routing, and adjusting fraud rules are common strategies.

How often should payment metrics be reviewed?

Payment performance should be monitored in real time with weekly reviews to identify trends and respond to issues quickly.

Can Biyo POS improve payment success?

Yes. Biyo POS offers smart payment routing, fraud prevention tools, and analytics dashboards that help businesses increase payment approval rates and improve checkout performance.