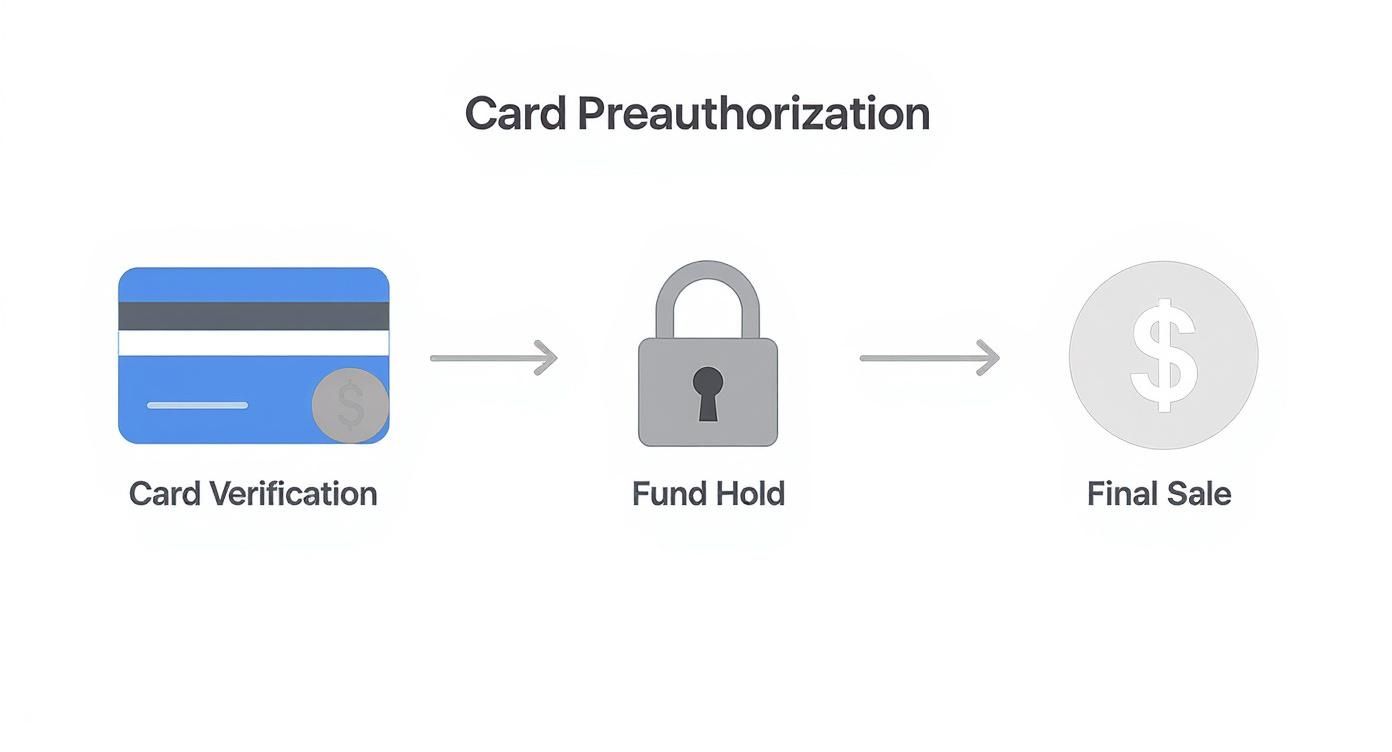

Ever noticed a “pending” charge on your card after booking a hotel or renting a car? That’s a credit card preauthorization at work. It’s a temporary hold placed on a customer’s card to verify validity and reserve funds before the final amount is known.

No money is actually transferred at that stage. Instead, the bank reduces the customer’s available credit by a specific amount while the merchant decides whether to finalize, adjust, or cancel the transaction.

For businesses, this mechanism is not just convenient — it is strategic risk management.

Unlocking the Value of Credit Card Preauthorization

At its core, a credit card preauthorization functions as a financial safeguard. It confirms available funds before goods are delivered or services are completed. That confirmation dramatically reduces payment uncertainty.

Industries that rely heavily on preauthorization include:

* Hospitality

* Car rentals

* Fuel stations

* Restaurants and bars

* E-commerce (especially delayed shipment models)

With global card transaction volumes projected to surpass $3.8 trillion in the coming years, the importance of secure authorization workflows continues to grow. Fraud prevention systems have reduced payment fraud significantly in sectors where authorization controls are standard, underscoring how essential this first verification step has become.

A preauthorization creates operational confidence. It reduces declined payments, limits disputes, and provides a structured workflow for transactions where final totals vary.

Why Preauthorization Is a Business Essential

Preauthorization protects revenue in three critical ways:

1. Payment Verification

It confirms the card is active and has sufficient credit before services are rendered.

2. Revenue Protection

Funds are reserved for future charges such as incidentals, add-ons, or variable pricing components.

3. Fraud Mitigation

Successful authorization validates the issuing bank’s approval, creating documented proof of cardholder consent.

This step is especially valuable in high-ticket or variable-amount environments. A business that operates without authorization controls assumes unnecessary risk exposure.

Preauthorization vs Final Sale at a Glance

| Feature | Credit Card Preauthorization | Final Sale (Capture) |

|---|---|---|

| Purpose | Verify funds and place temporary hold. | Transfer funds permanently to merchant. |

| Customer Account | Appears as pending; reduces available credit. | Appears as posted charge. |

| Duration | Temporary (typically 3–7 days). | Permanent once settled. |

| Merchant Flexibility | Can capture, adjust, void, or allow expiration. | Requires refund to reverse. |

| Risk Level | Low — funds are reserved. | Transaction completed. |

The distinction is operationally important. Authorization reserves funds; capture moves funds.

How a Credit Card Transaction Actually Works

Every card payment follows three stages: Authorization, Capture, and Settlement.

Stage 1: Authorization

The POS sends a request to the issuing bank asking whether funds are available. If approved:

* An authorization code is issued

* A temporary hold is placed

* Funds remain in the customer’s account but are unavailable

If declined, the transaction stops immediately.

Stage 2: Capture

Capture converts the hold into a finalized transaction. This step typically occurs:

* At checkout (hotels)

* When closing a tab (restaurants)

* After final service completion (rentals)

The flexibility between authorization and capture is what makes preauthorization powerful. Adjustments can be made before funds are permanently transferred.

Stage 3: Settlement

During settlement:

* Funds move from the customer’s bank

* Card networks process the batch

* The merchant receives payment (minus fees)

Settlement typically occurs in daily processing cycles.

Where Preauthorizations Shine in Everyday Business

Preauthorization solves payment uncertainty across industries.

Credit card usage continues to expand, exceeding $1 trillion per quarter in the U.S. alone. With card payments now representing a significant share of consumer transactions, businesses must proactively manage authorization risk.

Hotels and Hospitality

Hotels preauthorize:

* Room rate

* Taxes

* Incidentals

If no additional charges occur, only the final amount is captured and the remainder is released.

Car Rentals

Rental agencies place larger holds to cover:

* Rental fees

* Fuel charges

* Toll fees

* Damage deposits

This reduces exposure to unpaid liabilities.

Restaurants and Bars

Opening a tab typically involves a small authorization (often $1 or a preset amount). The final bill, including tip, is captured when the tab closes.

Fuel Stations

Pay-at-the-pump systems preauthorize a fixed amount (e.g., $75–$150). Once fueling ends, the system captures the actual fuel cost and releases the difference.

Managing Authorization Holds and Customer Communication

Most disputes stem from misunderstanding — not fraud.

Clear communication prevents:

* Customer confusion

* Support calls

* Chargebacks

Typical hold durations vary by industry:

Typical Preauthorization Hold Durations by Industry

| Industry | Common Hold Duration | Purpose |

|---|---|---|

| Hotels | Stay duration + 3–7 days | Room and incidentals |

| Car Rentals | Rental period + 5–10 days | Security deposit |

| Restaurants (Tabs) | 1–5 hours | Open tab validation |

| Gas Stations | 1–4 days | Fuel authorization buffer |

| Online Retail | 1–5 business days | Shipment verification |

Training staff to explain that a pending transaction is a temporary hold dramatically reduces unnecessary disputes.

How Preauthorization Reduces Chargebacks

Chargebacks damage merchant accounts and increase processing costs.

Preauthorization reduces chargeback exposure by:

* Verifying cardholder approval upfront

* Documenting authorization codes

* Confirming sufficient funds

With card usage projected to grow substantially in the coming years, proactive authorization management protects long-term merchant stability.

For merchants seeking deeper risk management strategies, understanding the mechanics of chargebacks is essential.

Setting Up Preauthorization on Your POS

Most modern POS systems include an “Authorization Only” or “Preauth” option in payment settings.

Implementation steps:

1. Enable authorization-only settings.

2. Train staff on authorization vs capture.

3. Monitor open authorizations daily.

4. Void unused holds promptly.

5. Reconcile captured transactions in end-of-day reports.

Operational discipline ensures no revenue gaps and no expired authorizations.

Frequently Asked Questions

What happens if a preauthorization expires?

If not captured within the authorization window (usually 5–7 days), the hold expires automatically and funds return to the customer’s available balance. A new transaction would be required.

Can customers see a preauthorization?

Yes. It appears as a pending charge on their statement but is not finalized until captured.

Can a merchant cancel a preauthorization?

Yes. Merchants can void the authorization, which signals the issuing bank to release the hold.

Is preauthorization the same as prepayment?

No. Preauthorization reserves funds temporarily. Prepayment immediately transfers funds to the merchant.

Does preauthorization reduce fraud?

Yes. It confirms bank approval and available funds before services are provided, lowering fraud risk and minimizing chargebacks.

Managing credit card preauthorization effectively protects revenue, reduces disputes, and strengthens customer trust. Businesses that integrate authorization workflows into their POS strategy operate with greater financial certainty and lower risk exposure.

If you want streamlined authorization controls, real-time reporting, and dispute reduction tools, explore how Biyo POS simplifies payment management from authorization to settlement.