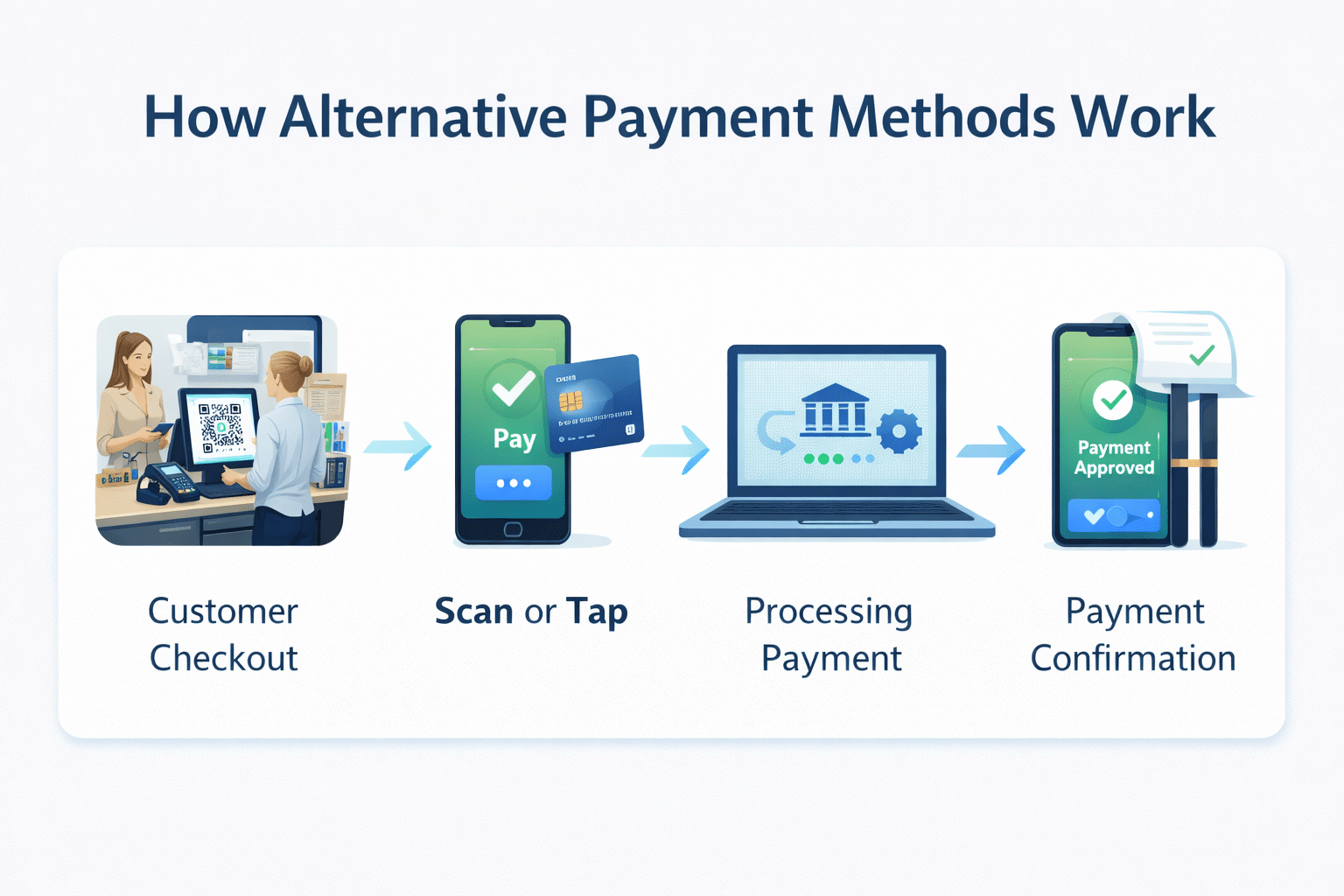

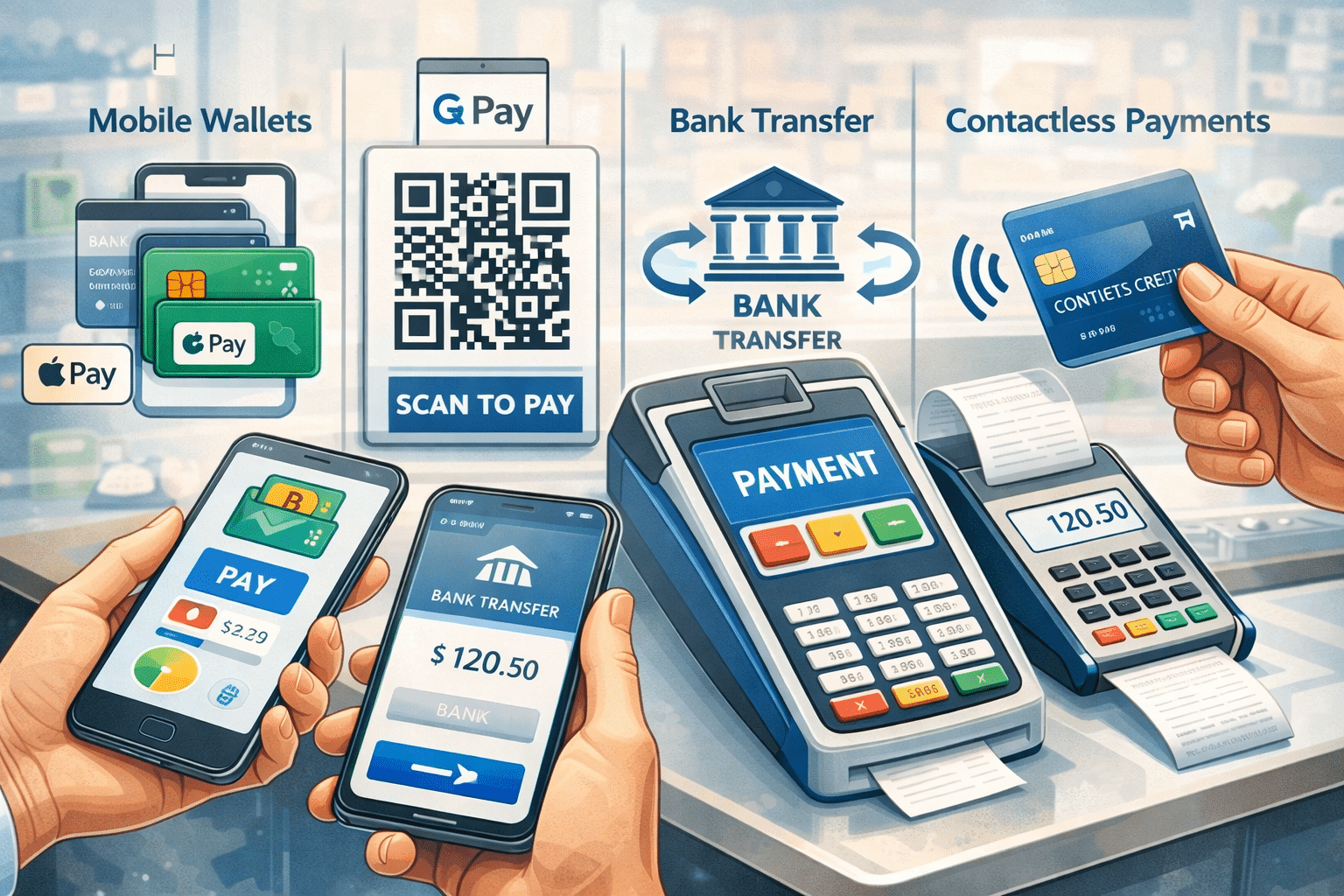

What are alternative payment methods, and why have they become such a critical part of today’s business landscape? Simply put, what are alternative payment methods refers to any way consumers and businesses exchange money outside of traditional cash or standard credit and debit cards. These payment options include mobile wallets, digital wallets, contactless payments, QR code payments, ACH transfers, bank transfers, buy now pay later options, cryptocurrency payments, prepaid cards, gift cards, and peer-to-peer payments.

As commerce continues to shift toward digital-first experiences, what are alternative payment methods is no longer a technical question reserved for finance teams. Instead, it is a practical concern for business owners, operators, and customers alike. Consumers expect speed, flexibility, and convenience at checkout, while businesses want lower costs, faster settlements, and better data visibility. Understanding what are alternative payment methods helps bridge that gap and ensures smoother transactions on both sides.

Table of Contents

- Understanding the Definition and Scope

- Mobile and Digital Wallet Payments

- Bank Transfers and Account-to-Account Payments

- Flexible Checkout and Deferred Payment Options

- Emerging and Specialized Payment Technologies

- Frequently Asked Questions

Understanding the Definition and Scope

To fully understand what are alternative payment methods, it helps to look at how payment behavior has evolved over the past two decades. Cash once dominated everyday transactions, followed by widespread adoption of credit and debit cards. However, the rise of smartphones, eCommerce, and mobile banking apps transformed how people expect to pay.

Today, alternative payment methods represent a broad category of electronic payment methods designed to improve speed, accessibility, and user experience. These methods often remove physical barriers, reduce manual handling, and support fully cashless payment systems. As a result, they are now embedded in daily life rather than treated as optional add-ons.

What Makes a Payment Method “Alternative”

When asking what are alternative payment methods, the key distinction lies in how funds move and how users interact with the payment process. Alternative payment methods operate outside traditional cash handling and standard card-based networks. They typically rely on digital infrastructure, software platforms, or direct bank connectivity rather than physical exchange or card swipes.

For example, digital wallet payments store credentials securely within apps instead of physical wallets. Bank transfer payments move funds directly between accounts without card networks acting as intermediaries. Peer-to-peer payments allow individuals or businesses to exchange money using mobile apps rather than POS terminals. Each of these methods changes the flow of money in a meaningful way.

From an industry perspective, alternative payment methods often reduce friction and dependency on legacy systems. They enable faster innovation, easier integrations, and more flexibility for businesses. As technology continues to advance, the definition of what are alternative payment methods continues to expand rather than shrink.

Why Consumers Prefer Cashless Payment Systems

Consumers increasingly prefer cashless payment systems because they align with modern lifestyles centered around smartphones and digital tools. Carrying cash feels inconvenient when mobile payment options allow users to pay with a single tap or scan. This convenience becomes especially valuable in busy environments like restaurants, retail stores, and public transportation.

Security also plays a major role in adoption. Many alternative payment methods rely on encryption, tokenization, and biometric authentication such as fingerprints or facial recognition. These protections reduce the risk of theft compared to cash, which offers no recovery once lost. As a result, digital wallet payments often feel safer to everyday users.

Another factor driving preference is speed. Contactless payment methods and mobile wallets significantly reduce checkout time. When customers experience faster transactions repeatedly, those methods quickly become their default choice.

Why Businesses Are Shifting to Alternatives

Businesses adopt alternative payment methods primarily to meet customer expectations and improve operational efficiency. Faster checkout processes reduce lines, increase throughput, and improve the overall customer experience. In high-volume environments, even a few seconds saved per transaction can lead to measurable revenue gains.

Alternative payment methods also improve record keeping and financial visibility. Electronic payment methods automatically generate transaction data, making reconciliation, reporting, and auditing easier. This data-driven insight helps businesses make better decisions about pricing, inventory, and staffing.

From a competitive standpoint, offering modern payment options signals credibility and professionalism. Customers often associate flexible payment choices with well-run businesses, which strengthens brand trust and long-term loyalty.

Mobile and Digital Wallet Payments

Mobile and digital wallet payments sit at the center of discussions around what are alternative payment methods. These tools store payment credentials securely on smartphones, tablets, or wearable devices, allowing users to complete transactions without physical cards or cash.

Digital wallets also extend beyond payments by supporting receipts, loyalty programs, and promotions. This combination of functionality explains why mobile wallets have become one of the fastest-growing mobile payment options worldwide.

How Mobile Wallets Work

Mobile wallets function by storing encrypted payment credentials within a secure application. When a customer initiates a transaction, the wallet communicates with the payment terminal using NFC payments or QR code payments. Instead of transmitting raw card data, the system sends a one-time encrypted token that protects sensitive information.

Most mobile wallets link directly to bank accounts or existing cards, which means users do not need to preload balances in most cases. This setup reduces friction during onboarding and encourages widespread adoption. Once configured, payments take only seconds to complete.

From a business perspective, mobile wallets integrate seamlessly with modern POS systems. They reduce manual errors, speed up checkout, and support contactless payment methods that customers increasingly expect.

Benefits of Digital Wallet Payments

Digital wallet payments significantly reduce checkout time compared to traditional card entry or cash handling. Customers simply tap their device or confirm a transaction within an app. This speed becomes especially valuable during peak hours when long lines can hurt customer satisfaction.

Another major benefit lies in enhanced security. Digital wallets rely on tokenization and device-level authentication, which limits exposure to fraud. Even if a device is lost, built-in security features protect stored credentials.

For businesses, digital wallets open doors to deeper customer engagement. Many wallets support loyalty rewards, targeted offers, and digital receipts, turning the payment moment into a marketing opportunity rather than a simple transaction.

Virtual Wallets and Contactless Payments

Virtual wallets operate entirely online and often power eCommerce, subscriptions, and digital services. These wallets store balances or payment credentials that customers can use across platforms. They reduce the need to repeatedly enter payment details, which lowers friction and cart abandonment.

Contactless payments rely on similar underlying technology but focus on in-person transactions. Customers tap a card or device instead of swiping or inserting it. This interaction feels faster and more intuitive, especially for younger consumers.

Together, virtual wallets and contactless payments redefine what are alternative payment methods by blending convenience, speed, and security into a single experience.

Bank Transfers and Account-to-Account Payments

Bank-based payment options represent a foundational category when exploring what are alternative payment methods. These methods move money directly between bank accounts without relying on card networks, which often results in lower fees and fewer intermediaries.

As financial institutions modernize their infrastructure, bank transfers and account-to-account payments have become faster and more accessible. This shift has made them increasingly attractive for both businesses and consumers.

ACH Transfers and eChecks

ACH transfers are electronic payments processed through established banking networks. They are commonly used for payroll, subscriptions, rent, and utility payments. While settlement typically takes one to three business days, ACH payments offer reliability and low processing costs.

eChecks operate similarly to ACH transfers but replace paper checks with digital authorization. Customers enter their bank details online, allowing funds to move electronically. This approach reduces errors, eliminates mailing delays, and improves record accuracy.

For businesses focused on recurring billing or large transactions, ACH payments provide a cost-effective alternative to card-based processing. They remain a key answer to what are alternative payment methods for predictable cash flow.

Instant Payments and Real-Time Transfers

Instant payments settle transactions within seconds rather than days. These systems rely on modern banking rails designed for real-time communication between financial institutions. Customers receive immediate confirmation that funds have moved successfully.

For businesses, real-time transfers improve cash flow management. Faster access to funds reduces reliance on credit lines and simplifies daily operations. This speed can be especially valuable for small businesses operating on tight margins.

As adoption expands, instant payments are reshaping expectations around what are alternative payment methods in both consumer and B2B environments.

Mobile Banking Apps and Bank Transfer Payments

Mobile banking apps allow users to initiate bank transfer payments directly from their smartphones. Many apps support peer-to-peer payments and account-to-account transfers with minimal effort. This familiarity encourages frequent use.

These apps reduce reliance on physical cards while lowering transaction costs for businesses. Customers appreciate the simplicity of paying directly from their bank without additional steps.

In many regions, mobile banking apps now define everyday digital payments, making them a core component of what are alternative payment methods.

Flexible Checkout and Deferred Payment Options

Flexible checkout models play a critical role in discussions about what are alternative payment methods. These options focus on giving customers more control over how and when they pay, which directly impacts purchasing decisions.

As prices rise and consumer budgets tighten, flexibility at checkout often determines whether a transaction is completed or abandoned.

Buy Now Pay Later Options

Buy now pay later options allow customers to split purchases into manageable installments while receiving goods immediately. This structure reduces the psychological barrier associated with large upfront costs. As a result, customers feel more confident completing purchases.

BNPL services often provide transparent repayment schedules and minimal approval steps. This clarity builds trust and reduces anxiety around hidden fees or interest. Many consumers view BNPL as more approachable than traditional credit.

For businesses, buy now pay later options increase conversion rates and average order values. They represent one of the fastest-growing segments within what are alternative payment methods.

Prepaid Cards and Gift Cards

Prepaid cards limit spending to a preloaded balance, which helps customers control budgets. They are commonly used for travel, corporate expenses, and personal spending management. This predictability benefits both users and merchants.

Gift cards act as stored value tied to a specific brand. When customers redeem gift cards, they often spend more than the card’s original value. This behavior drives incremental revenue.

Both prepaid cards and gift cards support cashless payment systems while strengthening customer retention and brand loyalty.

Peer-to-Peer Payments in Commerce

Peer-to-peer payments began as tools for sending money between friends and family. Over time, these platforms expanded into commercial use, allowing businesses to accept payments through familiar apps.

Customers enjoy the convenience of using apps they already trust. Payments typically settle quickly, which improves cash flow for merchants.

For small businesses and service providers, peer-to-peer payments offer a simple, low-cost entry point into digital payment acceptance.

Emerging and Specialized Payment Technologies

Emerging technologies continue to influence how businesses define what are alternative payment methods. These solutions often focus on automation, speed, and reduced dependency on traditional infrastructure.

While adoption varies by market, early adopters often gain competitive advantages by offering innovative payment experiences.

QR Code Payments and Scan-to-Pay

QR code payments allow customers to scan a code using their smartphone to complete transactions. This approach eliminates the need for physical payment terminals and reduces setup costs for businesses.

Scan-to-pay systems work especially well in fast-paced environments such as restaurants and events. Customers control the process, which reduces wait times and errors.

Because QR codes rely on devices customers already own, adoption continues to grow globally.

Cryptocurrency Payments

Cryptocurrency payments use blockchain technology to facilitate decentralized transactions. These payments appeal to customers seeking global accessibility and reduced reliance on traditional financial systems.

Price volatility remains a challenge, although stablecoins help mitigate this risk. Some businesses convert crypto payments into local currency immediately to avoid exposure.

While still niche, cryptocurrency payments continue influencing discussions around what are alternative payment methods.

Online Payment Alternatives and Future Trends

Online payment alternatives include embedded payment systems and API-driven platforms. These tools integrate payments directly into apps and websites, reducing visible checkout steps.

As payments become more seamless, customers focus on the experience rather than the transaction process. This shift improves satisfaction and loyalty.

Future trends will continue redefining what are alternative payment methods through automation, personalization, and invisible payments.

How Biyo POS Supports Alternative Payment Methods

:contentReference[oaicite:0]{index=0} helps businesses accept and manage alternative payment methods through one unified, cloud-based platform. From mobile wallets and contactless payments to ACH transfers and cashless payment systems, Biyo POS simplifies modern payment acceptance across retail and hospitality. With real-time reporting, flexible integrations, and intuitive checkout tools, Biyo POS makes it easier to support what are alternative payment methods at scale. You can schedule a call to see the platform in action or sign up to get started.

Frequently Asked Questions

What are alternative payment methods?

What are alternative payment methods refers to payment options beyond cash and traditional credit or debit cards. These include mobile wallets, bank transfers, QR code payments, buy now pay later options, and other electronic payment methods.

Are alternative payment methods secure?

Most alternative payment methods use encryption, tokenization, and authentication technologies. These measures often provide stronger security than cash-based transactions.

Do businesses need special hardware?

Some methods require NFC-enabled terminals, while others work through QR codes or online platforms. Many modern POS systems support both approaches.

Which industries benefit the most?

Retail, restaurants, eCommerce, and service businesses benefit from faster checkout, lower friction, and flexible payment options.

How can a business start accepting alternative payment methods?

Businesses can start by choosing a modern POS platform like Biyo POS that supports multiple payment options and enabling the methods their customers prefer.