When it comes to essential tips for managing cash flow in small business, it all boils down to three things: looking ahead to predict your money, keeping a close watch on it every day, and actively finding ways to make it work better for you.

Think of it as the lifeblood of your company. It’s the simple, but critical, act of tracking every dollar coming in and going out. This ensures you always have enough cash on hand to pay the bills, your staff, and yourself. This isn't just good accounting—it's the difference between merely surviving and truly thriving.

Why Cash Flow Management is Your Business Lifeline

Let’s get real for a moment: profit on paper means absolutely nothing if your bank account is empty. I've seen countless entrepreneurs learn this the hard way.

Imagine you just landed a huge client. Your profit-and-loss statement looks incredible. But here's the catch: you have to pay your suppliers and employees right now. That big check from your client? It might not show up for 30, 60, or even 90 days. This is the cash flow gap—a dangerous place where even profitable businesses can get into serious trouble.

Managing your cash flow isn't just about bookkeeping; it's about survival. It's the oxygen your business needs to breathe. Without it, everything else, from marketing to daily operations, starts to suffocate.

This is especially true for new businesses. The financial pressure is intense, and without a solid grip on cash, even a brilliant idea can run out of gas. It's a key reason so many promising ventures, from local boutiques to new eateries, struggle to keep their doors open. We've actually dived deep into this topic in our guide on how restaurants can navigate common failure points.

The Real-World Impact of Poor Cash Flow

When you ignore the flow of money, you end up putting out fires instead of building your business. You might find yourself scrambling to make payroll, pushing back payments to suppliers you depend on, or having to pass on a golden opportunity because the funds just aren't there.

These aren't just financial hiccups. They chip away at your reputation, hurt team morale, and add a ton of stress to your plate.

The core of a strong financial strategy isn't about reacting to crises. It's about building a proactive system that anticipates challenges and creates stability, giving you the freedom to focus on growth instead of just staying afloat.

This isn't a rare problem, either. Cash flow is a massive headache for small businesses. Data shows that nearly 39% of U.S. small businesses have less than a month's worth of cash reserves. They're living on the edge.

For brand-new companies, the situation is even more precarious. A staggering 20.7% of businesses under two years old have less than seven days of cash on hand. One unexpected bill could be all it takes to sink them.

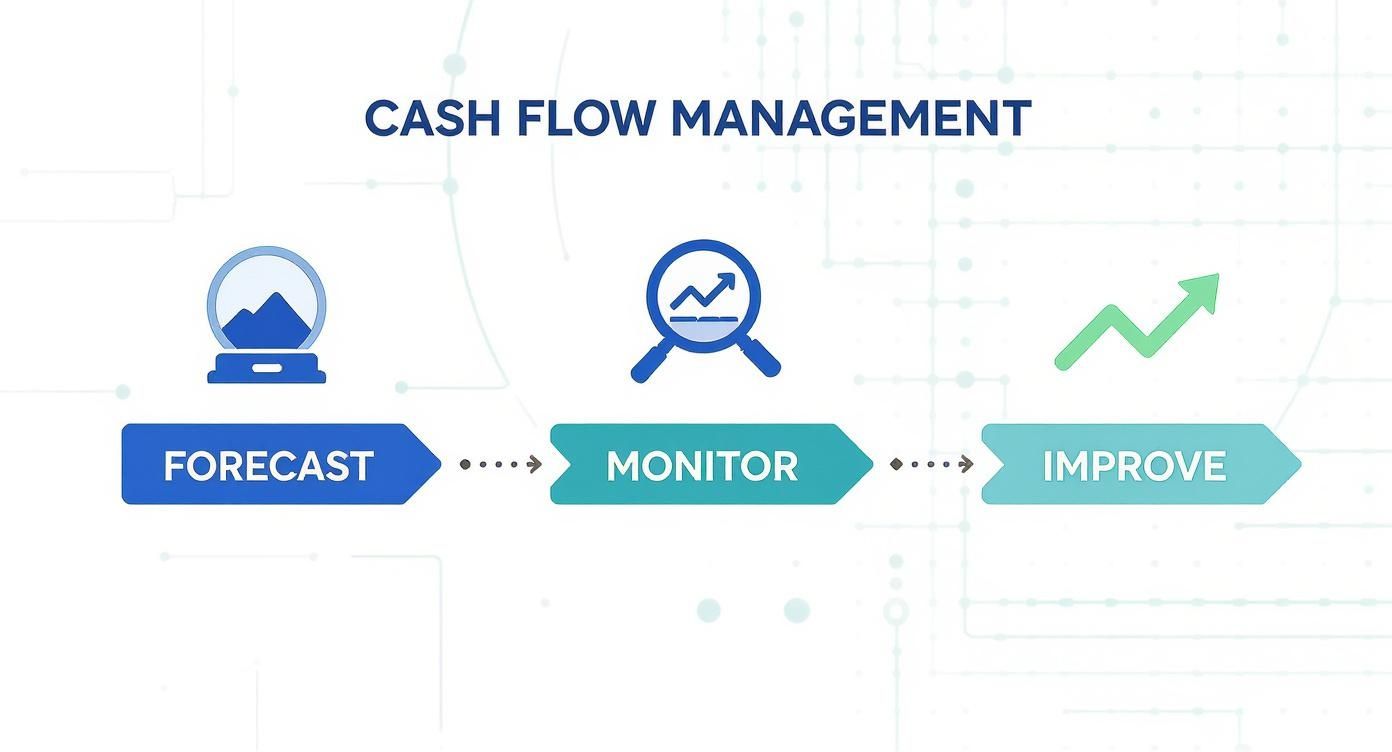

The Three Pillars of Financial Stability

To get out of this cycle of financial panic and into a position of control, your strategy needs to stand on three strong pillars:

- Forecasting: This is your financial roadmap. You're looking into the future to predict your cash inflows and outflows, which lets you spot potential shortfalls weeks or even months ahead of time.

- Monitoring: This is your daily check-up. It means tracking payments as they come in, keeping an eye on your bank balances, and generally knowing the financial pulse of your business at all times.

- Improving: This is where you take action. You actively work to get paid faster, manage your expenses wisely, and optimize the entire cycle to build a healthier, more resilient financial position.

By mastering these three areas, cash flow management stops being a chore and becomes your most powerful tool for building a business that lasts.

How to Build a Realistic Cash Flow Forecast

Staring at a blank spreadsheet can feel pretty intimidating, I get it. But building a cash flow forecast is less about complex accounting and more about good old-fashioned common sense. Think of it as your financial early-warning system. It’s not some document you create once and then file away to gather dust; it's a living, breathing guide that will genuinely transform how you make decisions for your business.

The whole idea is beautifully simple: map out the money you expect to come in and the money you know has to go out. When you do this realistically, you suddenly get the power to spot potential cash crunches weeks or even months down the road. That gives you precious time to react. It’s the difference between navigating a tricky road with a map versus doing it blindfolded.

This cycle is the heart of it all. You forecast, you monitor what’s actually happening, and then you act to improve things. It's a continuous loop.

As you can see, that forecast is the critical first step. It's where you start to take back control.

Projecting Your Cash Inflows

First up, let's figure out all the cash coming into the business. This isn't the time for wishful thinking. Your best friend here is historical data. Pull up your sales reports from last year and start looking for the patterns.

For instance, a coffee shop owner I know always sees a 20% spike in sales during the colder winter months, followed by a predictable dip in the heat of mid-summer. If she ignored that seasonality, her forecast would be useless. Your projections have to reflect these real-world ebbs and flows.

And remember, it's not just about sales. Make a list of every possible source of cash.

- Sales Revenue: Dig into your past sales data. If you're brand new, you'll have to rely on solid market research and start with a conservative estimate.

- Loan Payments: Are you expecting funds from an approved business loan to land in your account? Put it on the forecast.

- Asset Sales: Planning to sell that old piece of equipment that's been sitting in the back? Add that cash to the month you expect the deal to close.

- Owner Investments: If you plan to inject some of your own money into the business, make sure you account for it here.

Reliable forecasting is built on a foundation of clean, accurate records. The principles discussed in our guide on mastering bookkeeping for restaurant success are universal and will help any small business owner get their data in order for this very task.

Mapping Out Your Cash Outflows

Alright, now it’s time to get brutally honest about your expenses. This is where so many business owners trip up, underestimating their costs and setting themselves up for a nasty surprise. To keep it organized, I always split outflows into two buckets.

Fixed Costs are the predictable bills that hit your account every single month, no matter how busy you are. These are the easy ones.

- Rent or mortgage payments

- Salaries for your full-time staff

- Insurance premiums

- Monthly software subscriptions

- Loan repayments

Variable Costs are the ones that move up and down with your business activity. Think sales volume or production levels. These take a little more thought.

- Inventory and your cost of goods sold (COGS)

- Hourly wages and payments to contractors

- Shipping and delivery fees

- Your marketing and ad spend

- Utilities (which can definitely have their own seasonal swings)

One of the most common mistakes I see is business owners forgetting about the one-off or irregular expenses. Think about that big annual software renewal, your quarterly tax payments, or the potential for equipment to break down. It’s always smart to build a small buffer into your forecast for "unexpected costs"—it's a safety net you'll be glad you have.

Putting It All Together: A Simple Forecasting Template

To get you started, here is a very basic template. The goal isn't to capture every single detail right away, but to build the habit of thinking in terms of inflows and outflows over time. You can make this as detailed as you need, but even a simple version is a huge step forward.

Simple Cash Flow Forecasting Template

| Category | Month 1 (Projected) | Month 2 (Projected) | Month 3 (Projected) |

|---|---|---|---|

| Beginning Cash Balance | $5,000 | $4,550 | $5,100 |

| Cash Inflows | |||

| Sales Revenue | $10,000 | $12,000 | $11,500 |

| Asset Sale | $500 | $0 | $0 |

| Total Inflows | $10,500 | $12,000 | $11,500 |

| Cash Outflows | |||

| Rent | $2,000 | $2,000 | $2,000 |

| Payroll | $4,500 | $4,750 | $4,750 |

| Inventory/COGS | $3,000 | $3,500 | $3,200 |

| Marketing | $500 | $700 | $600 |

| Utilities | $300 | $350 | $350 |

| Other Expenses | $650 | $150 | $400 |

| Total Outflows | $10,950 | $11,450 | $11,300 |

| Net Cash Flow (Inflows – Outflows) | -$450 | $550 | $200 |

| Ending Cash Balance | $4,550 | $5,100 | $5,300 |

As you fill this out, you'll immediately see where your cash position is heading. That first month shows a small deficit, but knowing that ahead of time allows you to make adjustments before it becomes a problem.

Embrace the Rolling 12-Week Forecast

While an annual forecast is great for big-picture planning, a rolling 12-week forecast is your most powerful weapon for managing cash flow in a small business. Forget static documents. This is a dynamic spreadsheet that you live in and update every single week.

Here’s the rhythm: At the end of each week, you tack a new week onto the end of your forecast and, crucially, you update the previous weeks with your actual numbers. This simple habit keeps your financial horizon constantly in view.

If your updated forecast shows a potential cash shortfall five weeks from now, you won't be blindsided. You have more than a month to take action—maybe you start pushing clients to pay outstanding invoices, renegotiate payment terms with a supplier, or run a flash sale to juice your short-term revenue. This proactive approach turns your forecast from a boring report into your most valuable strategic tool.

Proven Strategies to Accelerate Your Cash Inflow

Having a detailed forecast is like having a map, but now it's time to actually direct the traffic and get cash flowing into your business faster. Improving your cash inflow is so much more than just sending out invoices and hoping for the best. It’s about building a proactive system that encourages prompt payment and creates a revenue stream you can actually count on.

Let's be honest: a business can look great on paper but still face a major crisis if payments trickle in too slowly. The real goal here is to shrink the gap between when you earn the money and when you can actually use it to pay your bills, your team, and invest in growth.

Modernize Your Payment and Invoicing Process

One of the simplest yet most powerful ways to speed things up is to make it incredibly easy for customers to pay you. If you're still relying on old-school, manual processes, you're creating friction and delays your business simply can't afford.

Start by offering a variety of ways to pay. Accepting online payments through credit cards, bank transfers (ACH), or digital wallets like Apple Pay can slash payment times compared to waiting for a check to arrive in the mail. When you integrate these options directly into your invoices or use a modern POS system, you make the whole transaction seamless—often just a single click for the customer.

Your invoicing habits also play a huge role. Don't wait until the end of the month to send everything out in a big batch.

- Invoice Immediately: Get that invoice out the door the moment the work is done or the product is delivered.

- Automate Reminders: Use your software to set up friendly, automated follow-up emails for invoices that are getting close to their due date or are already late.

- Ensure Clarity: Your invoice needs to be dead simple to understand, with a clear due date, an itemized list of charges, and straightforward payment instructions.

For a deeper dive, check out our guide on mastering invoices and payments for your business to really tighten up your billing cycle.

Create Incentives for Early Payments

Sometimes, all it takes is a little nudge to get your invoice moved to the top of a client's to-do list. Offering a small discount for paying early can be a surprisingly effective motivator.

Think about it this way: a freelance designer could offer "2/10, net 30" terms. This just means the client gets a 2% discount if they pay within 10 days; otherwise, the full amount is due in 30 days. On a $5,000 project, that's a $100 savings for the client. For you, it means guaranteed cash in the bank almost three weeks sooner. That tiny hit to your profit margin is often well worth the massive improvement to your cash flow.

Remember, the goal is to make paying you a priority. A small discount often provides a better return than the time and stress spent chasing down a late payment weeks or months later.

Secure Your Cash Flow Upfront

Why on earth should you wait until a project is finished to get paid? For any large project, custom order, or significant service, requiring a deposit is a standard—and essential—practice. It not only gives you an immediate cash injection but also confirms the client is serious and committed.

A web developer, for example, might require 50% of the project fee upfront and the final 50% upon completion. That initial payment helps cover immediate costs like software licenses or hiring a contractor, so you aren't funding the entire project out of your own pocket.

Likewise, a cafe taking a big catering order should absolutely get a deposit to cover the cost of ingredients. This protects the business from taking a huge loss if the customer cancels last minute.

Build Predictable, Recurring Revenue

One of the toughest parts of running a small business is the rollercoaster of unpredictable income. Shifting from a purely one-off transaction model to one with recurring revenue can create a stable financial foundation.

Here are a few ideas to get you started:

- Subscription Services: A local roaster could offer a monthly coffee bean subscription.

- Service Retainers: A marketing consultant could offer clients a monthly retainer for ongoing support instead of billing project by project.

- Tiered Pricing: A gym could offer Basic, Pro, and Premium membership levels with automatic monthly or annual billing.

This strategy transforms your revenue from a series of unpredictable peaks and valleys into a reliable monthly baseline. While over 74% of small businesses report having enough cash for at least one month's expenses, many are forced into tough situations when shortfalls hit. One survey found that 59% turn to business lines of credit and 53% delay paying themselves just to cope. You can find more insights on how small businesses navigate these financial trends on OnDeck.com. Building predictable income is one of the best ways to avoid having to make those painful choices.

Smart Tactics for Controlling Cash Outflow

Improving your cash flow isn't just about what you bring in; it’s about what you manage to keep. Mastering your expenses is a delicate balance—you have to trim the fat without cutting into the muscle that keeps your business growing. Honestly, getting a handle on your spending is one of the most direct ways you have to impact your cash flow.

Let's get into some practical, real-world ways to get a firm grip on your cash outflow, from big-picture strategies to the small, everyday adjustments that really add up.

Work With Your Suppliers on Payment Terms

Strong supplier relationships are gold, but that doesn't mean you can't be strategic about how and when you pay them. It’s pretty common practice to negotiate payment terms. If you're currently on Net 30, have you tried asking for Net 45 or even Net 60?

That simple change can give your business an extra 15 to 30 days of breathing room, helping you line up your payments with your incoming revenue. Imagine you're a retailer—this could mean paying for holiday inventory after the peak sales season, not before. You'd be surprised how many suppliers are willing to be flexible, especially for a reliable, long-term partner.

On the other hand, some vendors will offer you a discount for paying early. Always do the math. If the discount is big enough, it might be worth it, but only if you have a comfortable cash cushion to begin with.

Hunt Down and Eliminate "Ghost" Expenses

In a world full of subscriptions, it's dangerously easy to sign up for tools and software that seem essential at the moment but slowly become "ghost" expenses. That $20-a-month software you haven’t touched in six months is still quietly draining $240 a year from your account.

Set a calendar reminder every quarter to do a full-blown subscription audit. Go through your bank and credit card statements line by line and ask one simple question for each recurring charge: "Is this providing more value than it costs?" If the answer is no, or if you're not even sure, it's time to cancel. You can always sign back up later if you find you truly need it.

One of the biggest drains on cash is paying for things you don't actually use. A regular expense audit isn't just about cutting costs; it's about putting that cash back to work on things that actually help you grow.

Stop Letting Cash Get Trapped in Your Inventory

For any business selling physical products, inventory is a notorious cash trap. Every single item sitting on your shelf represents money that you can't use for payroll, marketing, or anything else. This is where smart inventory management becomes your secret weapon for healthy cash flow.

Stop guessing what you'll need and start using real data. A modern POS system gives you detailed sales reports that show what's flying off the shelves and what's gathering dust. With that information, you can:

- Avoid Overstocking: Cut back on orders for slow-moving products to free up cash.

- Prevent Stockouts: Make sure you always have enough of your bestsellers to meet demand so you never miss a sale.

- Try a "Just-in-Time" Approach: For some businesses, ordering inventory only as it's needed can drastically reduce how much cash is tied up in stock.

When you get your inventory right, you turn those physical goods back into liquid cash much more efficiently.

Think Twice Before Making Big Purchases

Dropping a huge amount of cash on new equipment or a company vehicle can put a massive dent in your reserves. Before you write that big check, take a moment to consider the alternatives.

Leasing expensive equipment is a fantastic option for preserving cash. Yes, the total cost over time might be a bit higher, but the low monthly payments are much gentler on your cash flow than one giant upfront expense.

And always ask yourself if a purchase is a "need" or a "want." Can you get by with a high-quality used piece of equipment instead of something brand new? Smart timing helps, too. If you can, plan major purchases for your busiest seasons when cash is flowing in, rather than during a slow period when every dollar is critical.

Make Technology Your Financial Co-Pilot

Let's be honest: juggling spreadsheets to track your cash flow is a nightmare. When you're busy with customers and day-to-day operations, it's way too easy to mistype a number or forget an update. One tiny mistake can throw off your entire forecast.

Ditching the manual tracking isn't just about saving a few hours. It’s about moving from a reactive, stressful chore to a proactive, strategic part of running your business. The right tech gives you a real-time, accurate picture of your financial health, so you're making decisions based on what’s happening now, not last month.

Get on Board with Modern Accounting Software

Modern accounting software is a true game-changer for small business owners. These platforms automatically sync with your bank accounts, credit cards, and payment processors, practically eliminating the human error that makes spreadsheets so risky.

Suddenly, you have an up-to-the-minute view of your cash position. You can instantly see which invoices are overdue, track expenses as they happen, and pull detailed financial reports in a few clicks. This isn't just about convenience; it’s about getting the clarity you need to stop putting out financial fires and start making smart, data-driven moves. It’s worth taking a moment to understand how technology transforms small business bookkeeping.

Your POS is More Than a Till—It's Your Command Center

For any retail or service business, your Point of Sale (POS) system is one of the most powerful tools you own. Think of it less like a cash register and more like the central nervous system for your entire operation. It's where sales, inventory, and customer data all come together.

A modern system like Biyo POS automates all your daily sales reporting, so you know exactly how much you've made without spending hours counting receipts. You can see what’s selling, when it’s selling, and even who’s buying it. That kind of detailed information is gold for building an accurate cash flow forecast.

The dashboard in Biyo POS gives you that "at-a-glance" view of your business performance that every owner craves.

With a quick look, you can see key metrics like total sales, number of transactions, and popular payment methods. This makes it easy to spot trends as they happen and make adjustments on the fly.

How Your POS Directly Boosts Cash Flow

Beyond just tracking sales, a good POS system actively improves your cash flow in a few crucial ways:

- Get Paid Faster: Integrated payment processing means money from card sales hits your bank account quicker. No more waiting days for funds to clear or wrestling with manual reconciliations.

- Smarter Inventory Spending: Real-time sales tracking helps you nail your stock levels. You can stop tying up cash in products that don't sell and make sure you never run out of your bestsellers.

- One Source of Truth: Your POS consolidates all your sales data. This can then sync directly with your accounting software, giving you a complete, seamless picture of your finances.

When your tech works together, it turns a bunch of disconnected data points into a clear story about your business’s health. That’s what gives you the confidence to make smarter, more profitable decisions.

It’s shocking, but an estimated 70% of small businesses still use old-school spreadsheets for their cash flow. We know this method is loaded with risks and inefficiencies. Making the switch to specialized software is one of the single most impactful things you can do to get a real handle on your money, plug revenue leaks, and find new ways to save.

Your Top Cash Flow Questions, Answered

Even the most seasoned business owners run into cash flow questions. Let's be honest, it's a tricky part of running a company. Here are some of the most common ones I hear, with straightforward answers to help you get a better handle on your finances.

How Often Should I Really Be Looking at My Cash Flow?

For most small businesses, a weekly review is the sweet spot. Think of it as a quick financial health check-up. It's frequent enough to spot a potential problem before it spirals out of control, but not so often that it becomes a burden.

This weekly glance lets you see who's paid up, what bills are coming due, and if any surprise expenses have hit your account. If you’re in a high-growth phase or your business is super seasonal (like a summer ice cream shop), you might even want to take a peek daily.

At an absolute minimum, you need to be doing a monthly review. But waiting that long is like looking in the rearview mirror—you're reacting to things that happened weeks ago. With modern accounting software, a weekly check-in can take just a few minutes, and it's time well spent.

What’s the Real Difference Between Profit and Cash Flow?

This is a big one, and it trips up so many entrepreneurs. It’s simple, but critical: Profit is what's left after you subtract expenses from revenue on paper. Cash flow is the actual, tangible money moving in and out of your bank account.

You can be wildly profitable and still go broke.

Imagine you're a graphic designer who just finished a huge project and sent an invoice for $10,000. Your profit-and-loss statement looks amazing—you've made a great profit! But you don't actually have that cash until the client pays you, and they might take 60 days. In the meantime, you still have to pay for your software, your rent, and yourself with real money. Profit is a theory; cash is the reality that keeps the lights on.

What Are the Most Important KPIs for Cash Flow?

You don't need to get lost in a sea of spreadsheets to know how you're doing. Focusing on just a few key performance indicators (KPIs) can tell you a powerful story about your financial efficiency.

- Days Sales Outstanding (DSO): This tells you, on average, how many days it takes for customers to pay you after you make a sale. A lower number is your goal—it means cash is getting into your hands faster.

- Days Payable Outstanding (DPO): This measures how long you take to pay your own suppliers. A higher number can be good for your cash position, but play this card carefully. You never want to damage a good relationship with a key vendor by paying too late.

- Cash Conversion Cycle (CCC): This is the master metric that ties the others together. It measures the total time it takes for a dollar you invest in inventory or resources to make its way back into your bank account as cash from a sale. The shorter the cycle, the more efficient your business is.

Keeping an eye on these three gives you a fantastic, high-level snapshot of how well you're managing the cash moving through your business.

I’m in a Pinch. What Are the Fastest Ways to Generate Cash?

When an unexpected cash crunch hits, you need to act, not panic. Taking clear, immediate steps can make all the difference.

Here are a few moves to make when you're in a tight spot:

- Get on the Phone with Overdue Accounts: Start with the biggest and oldest invoices. A personal call is a lot harder to ignore than another automated email reminder.

- Run a Flash Sale: Offer a compelling, limited-time deal on your most popular items or services. This can create a quick surge of much-needed revenue.

- Look into Invoice Financing: Some services will advance you a percentage of your unpaid invoices for a fee. It's not free money, but in a real emergency, it can be a lifesaver.

- Use Your Line of Credit: If you have a business line of credit, this is exactly what it’s for. It’s designed to help you bridge these kinds of short-term gaps.

- Review and Delay Payments: Comb through your upcoming bills. Can you postpone a payment for a non-critical tool? Could you ask a friendly vendor for a short extension? Every little bit helps.

Ready to turn cash flow management from a source of stress into a strategic tool? Biyo POS provides the real-time data and faster payment options you need to feel confident about your finances. You can track sales trends, manage inventory more effectively, and get paid faster—all from one place.

Start your free 14-day trial today and see the difference for yourself.