Payment technology has evolved quickly, and businesses now face more choices than ever at checkout. Among the most common options, the debate around EMV Chip & PIN vs Mobile Wallet Payments continues to shape how merchants think about security, speed, and customer experience. Both methods aim to reduce fraud and streamline transactions, yet they work in very different ways.

For many businesses, choosing the right payment methods is no longer just about compliance. It directly affects checkout speed, customer satisfaction, and long-term scalability. Understanding how EMV Chip and PIN compares with mobile wallet payments helps merchants align payment strategies with customer expectations.

This article explores EMV Chip & PIN vs Mobile Wallet Payments in depth. You will learn how each method works, how they differ in transaction security, speed, and adoption, and which option fits best with modern payment environments.

Table of Contents

- Understanding EMV Chip & PIN Payments

- How Mobile Wallet Payments Work

- Payment Security and Fraud Protection

- Checkout Speed and Customer Experience

- Business Impact and Future Readiness

- How Biyo Helps Support Modern Payments

- Frequently Asked Questions

Understanding EMV Chip & PIN Payments

EMV Chip and PIN payments have become a global standard for card-present transactions. This method replaced magnetic stripe cards to reduce fraud and improve transaction security.

What EMV Chip and PIN Really Means

EMV stands for Europay, Mastercard, and Visa. The technology uses a small embedded chip that generates a unique transaction code for every payment.

When customers insert their card and enter a PIN, the terminal verifies both the card and the user. This process prevents duplicated card data from being reused.

In the context of EMV Chip & PIN vs Mobile Wallet Payments, EMV focuses on physical card security rather than device-based authentication.

Because each transaction uses dynamic data, stolen information becomes useless.

Why EMV Adoption Became Mandatory

Card networks shifted liability to merchants who failed to adopt EMV. As a result, businesses upgraded terminals to avoid fraud losses.

EMV Chip and PIN dramatically reduced counterfeit card fraud in card-present environments. Fraudsters found it harder to clone chip cards.

This shift made EMV a baseline requirement rather than a competitive advantage.

Compliance now represents table stakes for payment acceptance.

Limitations of EMV Chip and PIN

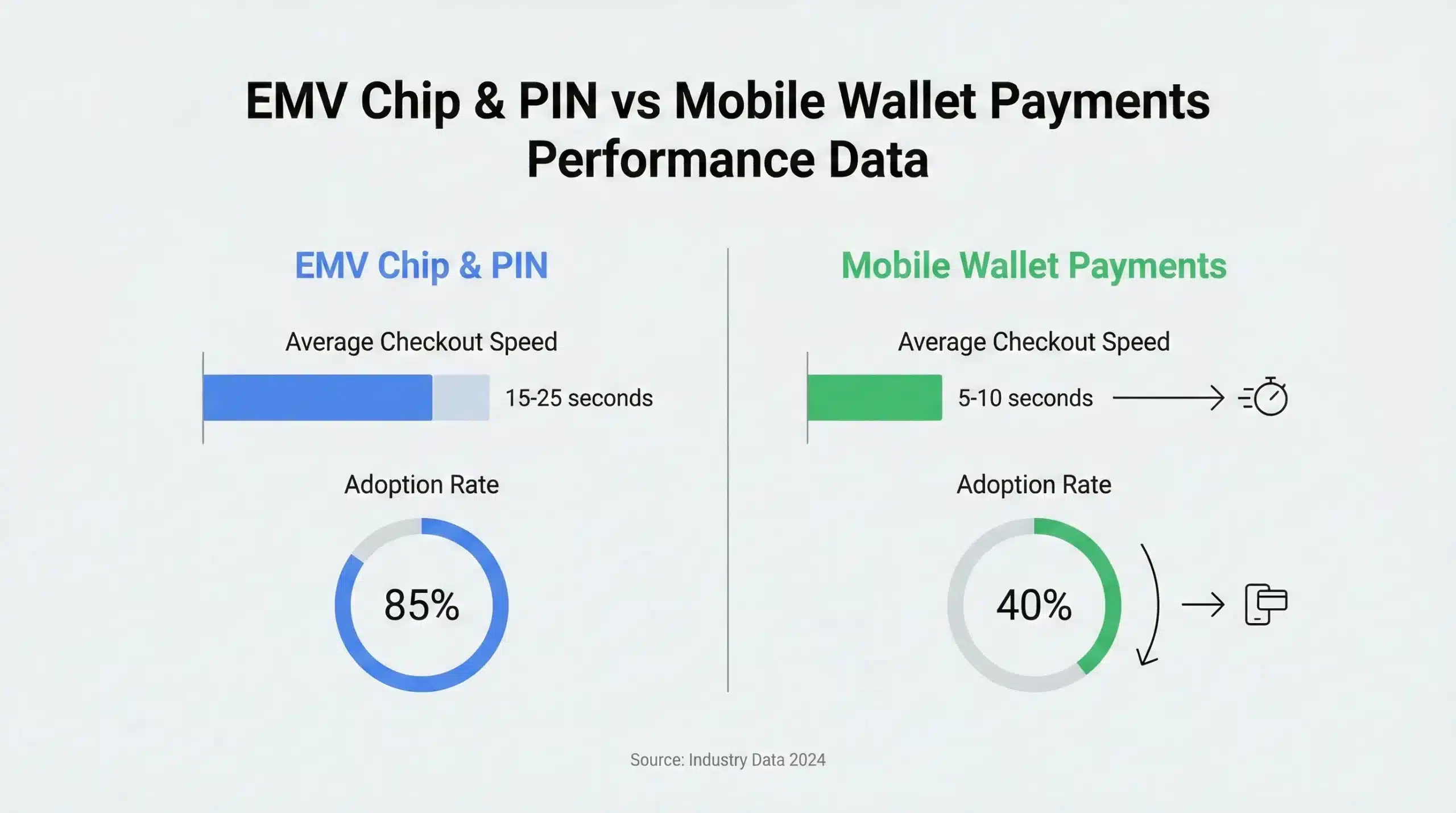

Despite strong security, EMV transactions take longer than swipe-based methods. Customers must insert cards and enter PINs.

Wear and tear on physical cards also causes failures. Damaged chips slow checkout and frustrate users.

As payment preferences change, these limitations influence the EMV Chip & PIN vs Mobile Wallet Payments discussion.

Speed and convenience increasingly matter.

How Mobile Wallet Payments Work

How Mobile Wallet Payments Work

How Mobile Wallet Payments Work

How Mobile Wallet Payments WorkMobile wallet payments rely on smartphones and wearable devices rather than physical cards. This approach has grown rapidly as contactless payments gain acceptance.

NFC Payments and Contactless Technology

Mobile wallets use Near Field Communication, or NFC, to transmit payment data securely. The device communicates with the terminal wirelessly.

Customers authenticate using biometrics or device passcodes. The transaction completes without inserting a card.

In the EMV Chip & PIN vs Mobile Wallet Payments comparison, NFC payments emphasize convenience and speed.

This approach reduces physical contact during checkout.

Apple Pay vs Chip Card Transactions

Apple Pay and similar wallets tokenize card data. Instead of sharing real card numbers, they use temporary digital tokens.

Even if intercepted, tokenized data cannot be reused. This adds another layer of protection.

When comparing Apple Pay vs chip card transactions, wallets often provide stronger protection against data theft.

Authentication remains device-specific.

Consumer Adoption of Mobile Wallets

Mobile wallet adoption varies by region and demographic. Younger consumers often prefer phone-based payments.

Contactless payments gained momentum due to convenience and hygiene concerns. Many users now expect this option.

As adoption grows, EMV Chip & PIN vs Mobile Wallet Payments becomes a question of readiness rather than replacement.

Businesses must support both.

Payment Security and Fraud Protection

Security remains central to payment decisions. Both EMV and mobile wallets aim to reduce fraud but use different methods.

Transaction Security in EMV Payments

EMV transactions rely on encrypted communication between the chip and terminal. Dynamic authentication protects each payment.

PIN verification adds another safeguard. Unauthorized users struggle to complete transactions.

This model works well for physical card security.

However, lost cards still present some risk.

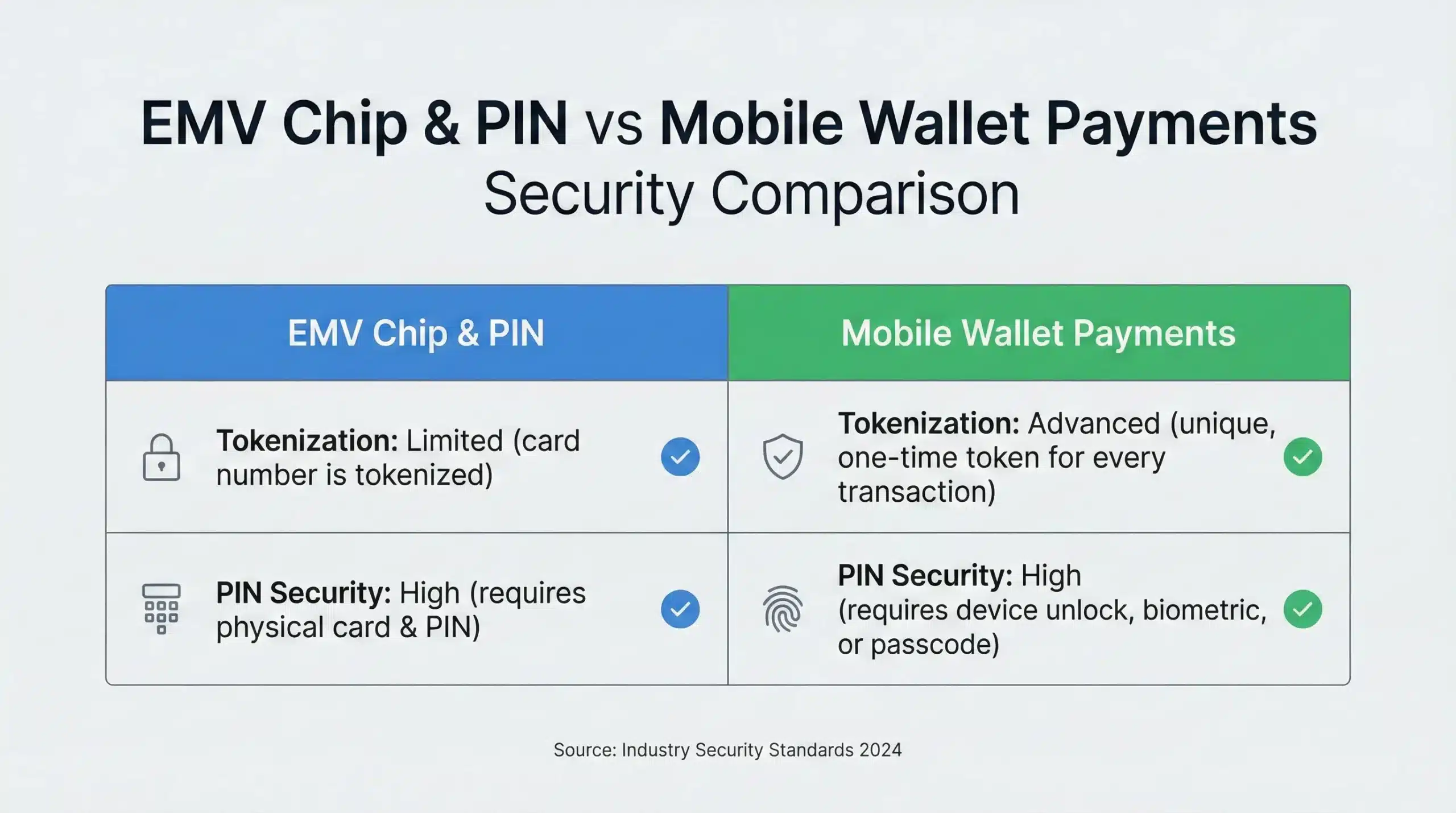

Tokenization and Device Security in Wallets

Mobile wallets replace card numbers with tokens. These tokens work only on specific devices.

Biometric authentication limits unauthorized use. Fingerprints and facial recognition add security.

In EMV Chip & PIN vs Mobile Wallet Payments, wallets often exceed traditional card security.

Stolen phones remain protected by device controls.

Fraud Trends and Risk Management

Fraud patterns shift as technology changes. Criminals target weaker channels.

As EMV reduced card-present fraud, online fraud increased. Mobile wallets further limit exposure.

Supporting modern payment methods helps businesses stay ahead of fraud trends.

Security evolves continuously.

Checkout Speed and Customer Experience

Speed and ease shape customer satisfaction. Payment methods influence line length and service flow.

Faster Checkout With Contactless Payments

Contactless payments complete in seconds. Customers tap and go.

This speed reduces queues during peak hours. Staff handle more transactions efficiently.

In EMV Chip & PIN vs Mobile Wallet Payments, speed often favors mobile wallets.

Shorter waits improve experience.

Customer Preferences and Expectations

Many customers expect modern payment options. Lack of contactless support frustrates them.

However, some still prefer physical cards. Habits vary.

Offering choice satisfies a wider audience.

Flexibility enhances perception.

Accessibility and Ease of Use

Mobile wallets simplify payments for users with disabilities. Biometric authentication removes PIN entry barriers.

EMV remains accessible but requires physical interaction.

Inclusive payment options support diverse customers.

Ease drives adoption.

Business Impact and Future Readiness

Payment decisions affect long-term operations. Businesses must balance cost, compliance, and growth.

Hardware and Infrastructure Requirements

EMV requires chip-capable terminals. Mobile wallets require NFC-enabled hardware.

Modern terminals often support both. Upgrading once covers future needs.

Investment now prevents repeated upgrades later.

Future-ready hardware saves money.

Operational Efficiency and Staff Training

Supporting multiple payment methods reduces friction. Staff adapt quickly.

Clear workflows prevent confusion at checkout.

Training remains minimal with intuitive systems.

Simplicity supports scale.

Preparing for Modern Payment Methods

Digital payments continue to evolve. Wearables and new wallets emerge.

Businesses that embrace flexibility stay competitive.

In EMV Chip & PIN vs Mobile Wallet Payments, adaptability matters most.

Future readiness drives growth.

How Biyo Helps Support Modern Payments

How Biyo Helps Support Modern Payments

How Biyo Helps Support Modern PaymentsBiyo POS supports both EMV Chip and PIN and mobile wallet payments, allowing businesses to offer secure and flexible checkout options. With NFC-enabled terminals, merchants can accept contactless payments without sacrificing compliance.

Real-time reporting and fast checkout workflows help reduce lines and improve transaction efficiency. Businesses gain insight into payment preferences and performance.

To see how Biyo can support modern payment strategies, you can schedule a call for a personalized walkthrough or sign up to get started.

Frequently Asked Questions

What is the main difference between EMV Chip & PIN and mobile wallet payments?

EMV relies on physical cards and PINs, while mobile wallets use devices, biometrics, and tokenization.

Are mobile wallet payments more secure than EMV?

Both are secure, but mobile wallets add tokenization and device-level authentication.

Do businesses need to choose one payment method?

No. Supporting both provides flexibility and meets customer expectations.

Are contactless payments faster than chip cards?

Yes. Contactless payments typically complete faster and reduce checkout time.

Does Biyo POS support both payment types?

Yes. Biyo POS supports EMV Chip and PIN along with mobile wallet and contactless payments.