Every business owner wants to maximize profits and minimize unnecessary expenses. One of the biggest hidden costs that can eat into your earnings is credit card processing fees. Learning how to reduce credit card processing fees can save your business hundreds or even thousands of dollars annually. By understanding how these fees work, comparing processors, and optimizing transactions, you can take control of your payment costs while improving your bottom line.

Table of Contents

- Understanding Credit Card Processing Fees

- Compare Payment Processors and Pricing Models

- Optimize Interchange Rates and Transactions

- Reduce Risk, Fraud, and Chargebacks

- Leverage POS Systems to Lower Processing Costs

- Save More with Biyo POS

- FAQ

Understanding Credit Card Processing Fees

Before you can learn how to reduce credit card processing fees, it’s crucial to understand what makes up these costs. Each transaction goes through multiple parties—banks, card networks, and payment processors—all of whom take a small cut. Knowing where these fees come from helps you identify where savings can be made.

Breakdown of Credit Card Processing Fees

Credit card processing fees typically include interchange fees, assessment fees, and processor markups. Interchange fees are paid to the card-issuing banks and usually make up the majority of your total costs. Assessment fees go to the credit card networks like Visa, Mastercard, or American Express for maintaining the infrastructure. Processor markups are the additional charges added by your payment processor for handling the transaction.

For example, on a $100 sale, you might pay around 2.9% or $2.90 in fees. Of that, roughly $1.80 could go to interchange, $0.15 to network assessment, and the rest to your processor. Understanding this structure allows you to identify which part is negotiable—usually, the processor’s markup—so you can begin optimizing costs more effectively.

Once you know how fees are divided, you can start tracking patterns and pinpoint where you might be overpaying. Regularly analyzing your merchant statements helps reveal trends like seasonal fluctuations or recurring surcharges that can be minimized through smarter payment routing or volume discounts.

Types of Pricing Models

Different pricing models impact your total cost in very different ways. The three most common structures are flat-rate pricing, tiered pricing, and interchange-plus pricing. Flat-rate pricing is simple to understand, as you pay a fixed percentage per transaction—popular among small businesses using services like Square. However, simplicity comes at a price, often higher than necessary for large volumes.

Tiered pricing groups transactions into “qualified,” “mid-qualified,” and “non-qualified” tiers based on risk and card type. Unfortunately, it lacks transparency, as you rarely see how a transaction is categorized or why you’re charged extra. Interchange-plus pricing, on the other hand, offers transparency by showing the exact interchange rate plus a fixed markup. This model is usually the most cost-effective for businesses processing higher volumes or mixed card types.

Understanding pricing structures helps you select a processor that aligns with your transaction profile. A restaurant, for instance, may benefit from interchange-plus pricing due to frequent small transactions, while an eCommerce business might prefer flat-rate pricing for predictability.

Hidden Fees You Should Watch For

Hidden fees are one of the biggest culprits behind inflated processing costs. Common examples include monthly statement fees, batch fees, PCI compliance fees, and gateway access charges. Even though each may seem minor—ranging from $5 to $25 monthly—they can add up to hundreds of dollars annually.

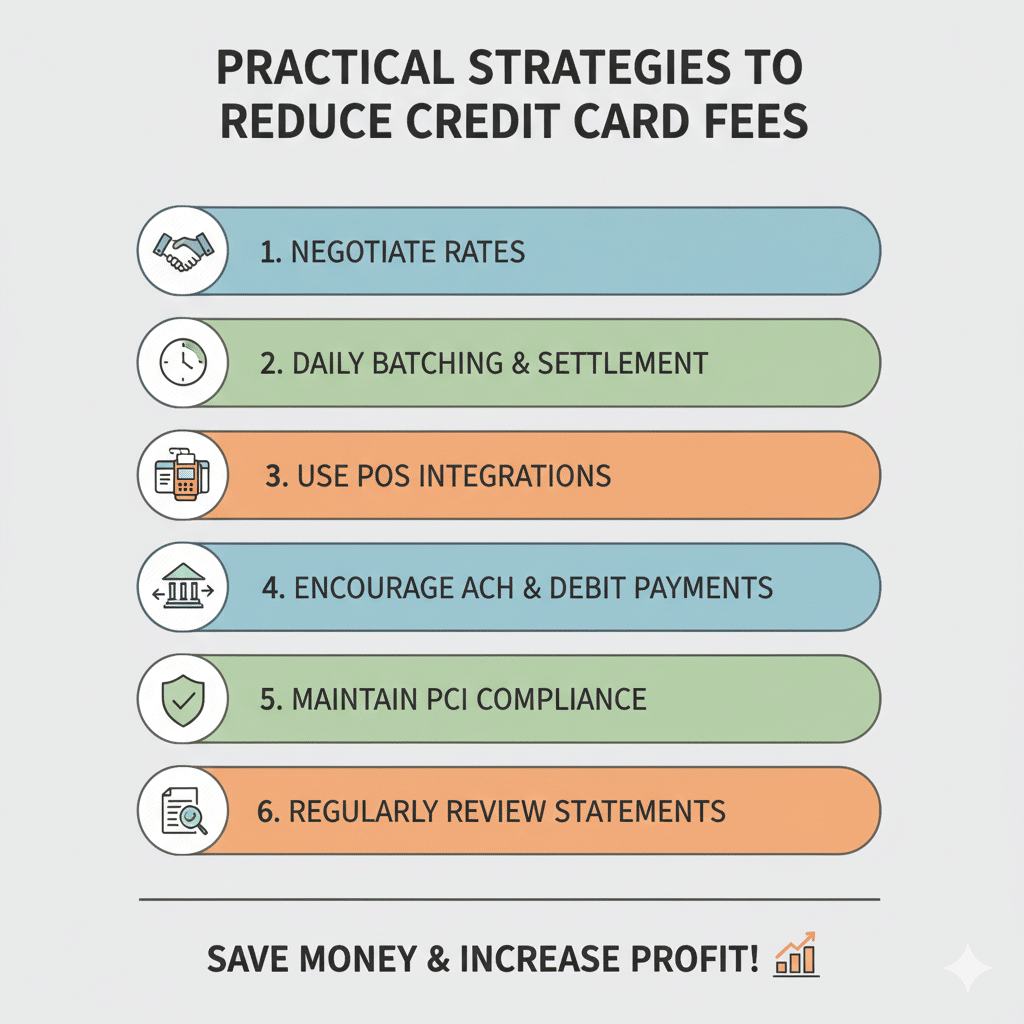

Review your processing statements line by line. If you find vague items labeled as “miscellaneous” or “service” fees, ask your provider for clarification. Some processors intentionally bury extra charges in their statements, banking on the assumption that merchants won’t scrutinize them. Removing or renegotiating these fees can result in instant savings.

It’s also essential to maintain PCI compliance to avoid extra monthly penalties. A non-compliance charge may add $20 or more per month, which is easily preventable by completing your annual compliance questionnaire and ensuring your POS meets the required security standards.

Compare Payment Processors and Pricing Models

Once you understand how credit card fees work, the next step is to compare payment processors and find one that offers fair pricing, flexible terms, and excellent support. Choosing the right processor can significantly reduce your overall payment costs.

Research and Compare Providers

When researching processors, don’t just focus on well-known names. Many lesser-known providers offer competitive rates with personalized customer support. Compare features such as interchange optimization, fraud protection tools, and integration with your current POS system. Look for transparent pricing, no long-term contracts, and clear service-level agreements.

Check customer reviews, case studies, and BBB ratings to gauge reliability. Ask potential processors if they support interchange-plus pricing or if they allow surcharging and cash discounting programs. This transparency is crucial for avoiding unexpected rate increases after signup.

Finally, consider the total value offered—not just the lowest rate. Fast deposits, responsive customer service, and reliable uptime can prevent costly delays and downtime. A good processor helps you maintain smooth cash flow and improve customer trust.

Negotiate Your Rates

Many business owners don’t realize that processing fees are negotiable. If your business has consistent sales and low chargeback rates, you hold bargaining power. Contact your provider and request a rate review, especially if your volume has grown since your contract began.

Ask for lower markup percentages, reduced monthly fees, or waived PCI fees. Use quotes from competitors as leverage. You can also request volume-based pricing if your monthly processing exceeds certain thresholds. Some processors automatically lower your fees when your monthly transaction volume crosses specific milestones.

If negotiations stall, don’t hesitate to switch. Just ensure your new processor offers a seamless migration process and integrates easily with your POS system. Switching to a transparent provider can lead to long-term cost reductions without affecting customer experience.

Consider Alternative Payment Methods

Encouraging customers to use lower-cost payment methods is a strategic way to cut fees. ACH transfers and debit cards generally cost less to process than credit cards since they bypass expensive network fees. If your business handles large invoices, consider adding ACH payment options to reduce costs.

Implementing surcharge programs—where a small fee is added to credit card payments—can offset costs, while offering a “cash discount” can motivate customers to pay with cash or debit. Just ensure your program complies with state laws and card network rules. Transparency at checkout is vital for maintaining customer satisfaction.

Alternative payment channels like mobile wallets or QR code payments can also save money when paired with optimized transaction routing. Some POS systems allow you to automatically route payments through the least expensive gateway per transaction type.

Optimize Interchange Rates and Transactions

Interchange optimization involves structuring your transactions to qualify for the lowest possible interchange rates. These rates are influenced by transaction type, payment method, and your business’s compliance practices.

Use Card-Present Transactions

Card-present transactions—where the card is physically tapped, inserted, or swiped—are generally cheaper because they carry less risk. Card-not-present transactions, such as phone or online orders, are more prone to fraud and therefore cost more. Encouraging customers to pay in person when possible can reduce your effective rate.

Invest in EMV and NFC-capable POS systems. EMV (chip) cards and contactless payments (like Apple Pay or Google Pay) provide strong encryption, lowering fraud risk and ensuring compliance. Many modern POS systems, such as Biyo POS, automatically detect the transaction type and apply the correct processing protocol to keep your rates low.

Even small operational adjustments—like avoiding manually keyed transactions—can make a measurable difference in your monthly processing costs. Keeping transactions “card-present” wherever possible is one of the simplest ways to save.

Batch Process Daily

Batching refers to closing out and submitting your daily transactions to the processor for settlement. When batches are delayed beyond 24 hours, transactions are considered higher risk and are reclassified at higher interchange rates. By batching daily, you ensure that all payments qualify for the best possible pricing tier.

Most modern POS systems can automate this process. Set your POS to batch automatically at the end of each business day. This reduces human error, prevents delays, and keeps your settlement times consistent.

Frequent batching also simplifies your bookkeeping, helping you maintain accurate daily revenue reports and ensuring predictable deposit schedules into your business bank account.

Ensure PCI Compliance

PCI compliance isn’t optional—it’s required for every business that handles cardholder data. Maintaining compliance protects both you and your customers while preventing penalty fees from your processor. Non-compliant businesses may be charged extra each month or risk suspension of their merchant accounts.

To stay compliant, use encrypted POS terminals, update your software regularly, and avoid storing unencrypted card data. Run vulnerability scans if required by your provider and maintain detailed security logs. Most processors provide free or discounted PCI self-assessment tools.

Being PCI compliant not only prevents fines but can also qualify you for lower processing rates under certain programs. It also strengthens your business’s reputation for secure transactions—a key factor for long-term customer trust.

Reduce Risk, Fraud, and Chargebacks

Reducing fraud and chargebacks not only protects your revenue but can also help you maintain lower processing fees. High-risk merchants pay more because they create additional liability for processors. By minimizing disputes and fraudulent transactions, you can preserve favorable rates and build trust with payment partners.

Implement Fraud Prevention Tools

Fraud prevention tools such as AVS (Address Verification Service), CVV checks, and 3D Secure authentication provide multiple layers of defense. These systems verify that the cardholder’s billing address, security code, and identity match the issuer’s records before approving transactions.

Modern POS systems integrate real-time fraud detection, analyzing transaction patterns and blocking suspicious behavior automatically. Using machine learning and rule-based triggers, these systems can identify anomalies such as multiple rapid purchases or mismatched IP locations.

Incorporating fraud prevention into your payment workflow reduces risk and improves your standing with processors, often resulting in lower long-term interchange rates and fewer chargeback-related costs.

Handle Chargebacks Quickly

When a customer disputes a transaction, time is of the essence. Every chargeback involves deadlines for providing evidence and communicating with banks. Delayed responses can result in automatic losses—even when the customer’s claim is invalid.

Keep detailed digital records for all transactions, including receipts, signed slips, and delivery confirmations. Use your POS system to store this data securely for quick retrieval. When notified of a chargeback, respond within 24–48 hours with clear documentation that proves the transaction’s legitimacy.

Quick, professional handling of chargebacks not only recovers lost revenue but also signals to your processor that you manage risk effectively—helping you maintain lower overall fees.

Encourage Customer Transparency

Clear communication is often the best defense against disputes. Display refund policies clearly at the point of sale, provide accurate receipts, and ensure that your business name appears consistently on card statements. Many chargebacks occur simply because a customer doesn’t recognize the merchant name on their bill.

Encourage customers to reach out directly with issues before contacting their bank. Train staff to handle refunds or exchanges promptly to prevent disputes from escalating. Proactive customer service goes a long way toward reducing chargeback ratios.

Transparency builds trust, minimizes conflicts, and keeps your business categorized as low-risk—resulting in more favorable rates and better long-term processor relationships.

Leverage POS Systems to Lower Processing Costs

Modern POS systems do far more than process payments—they can help reduce costs, automate optimization, and provide deep insights into your processing data. The right POS system is an essential ally in minimizing fees and improving efficiency.

Use POS Integration with Multiple Processors

Choosing a POS that supports multiple processors gives you flexibility and control over costs. For example, Biyo POS allows merchants to connect different payment gateways and choose the most cost-effective one for each transaction type. This process, called intelligent payment routing, ensures you always use the lowest-fee channel available.

Having multiple integrations also enhances your negotiation leverage. If one processor raises fees or changes contract terms, you can quickly shift your transactions elsewhere. This competition keeps rates fair and prevents vendor lock-in.

Such flexibility empowers businesses to respond dynamically to rate changes, seasonal volume shifts, or new processor promotions—ensuring continuous optimization without operational disruption.

Analyze Payment Statements with POS Reports

Detailed POS reports are crucial for identifying inefficiencies and potential savings. They reveal patterns such as high-cost card types, specific transaction methods triggering higher interchange rates, or unbatched sales. By monitoring this data, you can make informed adjustments.

Biyo POS offers robust reporting dashboards that allow merchants to analyze transaction data by processor, card type, and time period. This granular insight highlights exactly where you’re losing money and where improvements can be made.

With regular analysis, you can fine-tune operations, adjust pricing models, and maintain constant visibility into your financial performance—ensuring that no cent is wasted on unnecessary processing costs.

Offer Incentives for Low-Cost Payments

Incentivizing customers to use lower-cost payment methods can significantly reduce your processing burden. For instance, you can provide a small discount for debit or cash payments or include loyalty points for ACH transactions. Customers appreciate the transparency, and you benefit from lower fees.

Your POS can automate these incentives during checkout, applying discounts or bonuses automatically based on the payment method selected. This encourages a steady shift toward more affordable transaction types over time.

By gradually educating and incentivizing your customer base, you can create a win-win situation—your clients enjoy rewards, and your business maintains healthier profit margins.

Save More with Biyo POS

Managing payment fees doesn’t have to be complicated. Biyo POS helps businesses like yours optimize payment costs through smart routing, transparent reporting, and secure integration. The system supports interchange-plus pricing, daily batch automation, and PCI-compliant infrastructure. Whether you run a café, retail store, or restaurant, Biyo POS simplifies transaction management and minimizes overhead costs.

By using Biyo POS, you gain access to advanced features like payment routing, fraud prevention tools, and in-depth analytics—everything designed to help you reduce credit card processing fees. To explore how Biyo POS can transform your payment experience, schedule a call today.

Or, if you’re ready to start saving immediately, visit Biyo POS Signup to create your account and experience cost-efficient payment processing firsthand.

FAQ

1. What are the main ways to reduce credit card processing fees?

The most effective methods include negotiating with processors, choosing interchange-plus pricing, maintaining PCI compliance, and using POS systems with multiple processor integrations. Reviewing statements regularly also helps identify hidden or excessive fees.

2. How often should I analyze my merchant statements?

Experts recommend reviewing statements monthly. Regular analysis ensures that you catch changes in rates, detect hidden charges, and confirm that your negotiated terms remain consistent. Tools like Biyo POS make this process simple and efficient.

3. Can I legally pass credit card fees to customers?

Yes, in many regions, you can implement surcharge or cash discount programs, but it’s essential to comply with state and card network rules. Always display fee information transparently to avoid compliance issues.

4. Does switching processors impact my business operations?

Not necessarily. Most POS systems, including Biyo POS, make it easy to switch processors without downtime. The key is to plan transitions during off-hours and ensure all configurations are tested beforehand.

5. Are ACH payments really cheaper than credit card transactions?

Yes, ACH payments bypass card networks entirely, reducing interchange and network fees. They’re especially cost-effective for recurring or high-ticket transactions.