Imagine a crowded coffee shop during a busy lunch rush when the internet suddenly goes down. Customers are waiting in line, orders are piling up, and card payments should technically stop working. Yet somehow, businesses can still accept payments and continue operating normally.

That capability exists because of offline credit card transactions.

An offline credit card transaction allows businesses to process payments temporarily without a live internet connection. Instead of immediately contacting the customer’s bank for approval, the payment terminal securely stores the transaction information and forwards it for authorization once the internet connection is restored.

For modern businesses, offline payment capability has become extremely important.

Restaurants, retail stores, food trucks, pop-up events, airlines, festivals, and mobile businesses cannot afford to stop accepting payments every time network connectivity becomes unstable.

Without offline payment support, even a short internet outage could result in:

lost sales, frustrated customers, abandoned purchases, operational delays, and damaged customer experience.

Offline transaction systems solve this problem by helping businesses maintain continuity even during temporary connectivity issues.

However, offline payments also introduce additional risks and responsibilities.

Because the transaction is not verified instantly, businesses temporarily assume financial liability until the payment is officially approved later by the customer’s bank.

That means understanding how offline transactions work is essential for businesses that want to balance operational flexibility with financial security.

In this guide, we’ll explain what offline credit card transactions are, how the technology works behind the scenes, the difference between offline authorization methods, the risks businesses face, security protections involved, and best practices for safely managing offline payment processing.

Table of Contents

- What Are Offline Credit Card Transactions?

- How Offline Payments Work Technically

- Understanding Store-and-Forward Processing

- How EMV Offline Authentication Works

- The Journey of an Offline Payment

- Risks and Responsibilities for Businesses

- Security and PCI Compliance for Offline Payments

- Best Practices for Managing Offline Transactions

- Why Offline Payment Capability Matters More Than Ever

- How Biyo POS Helps Businesses Handle Offline Payments

- Frequently Asked Questions

What Are Offline Credit Card Transactions?

An offline credit card transaction is a payment processed without an active real-time internet connection to the customer’s bank.

Instead of instantly authorizing the payment online, the payment terminal temporarily stores the transaction data securely and submits it later when connectivity returns.

Offline transactions are commonly used during:

- Internet outages

- Wi-Fi disruptions

- Remote events

- Airline purchases

- Food truck operations

- Outdoor festivals

- Mobile business environments

For businesses, offline processing acts as a safety net.

Rather than stopping all card payments during connectivity problems, businesses can continue accepting sales and maintain normal operations.

This improves:

customer experience, operational continuity, and revenue protection.

Offline processing generally falls into two major categories:

- Store-and-forward transactions

- EMV offline authentication

Both methods allow businesses to accept payments without a live network connection, but they function differently behind the scenes.

How Offline Payments Work Technically

Offline payment processing depends on the payment terminal’s ability to securely capture, encrypt, and temporarily store transaction data.

Normally, online card transactions work by:

sending payment details instantly through payment processors to the customer’s issuing bank for approval.

However, when internet connectivity fails, the POS system cannot complete that real-time communication.

Instead, the terminal enters offline mode.

The device:

- Captures the card data

- Encrypts the information

- Stores the transaction locally

- Waits until connectivity returns

- Automatically forwards the transaction later

During this process, the terminal provides only a temporary approval.

The actual authorization from the bank still happens later once the stored transactions are transmitted online.

This delayed authorization creates both operational advantages and financial risks.

Modern POS systems are specifically designed to handle these situations securely while minimizing disruption during outages.

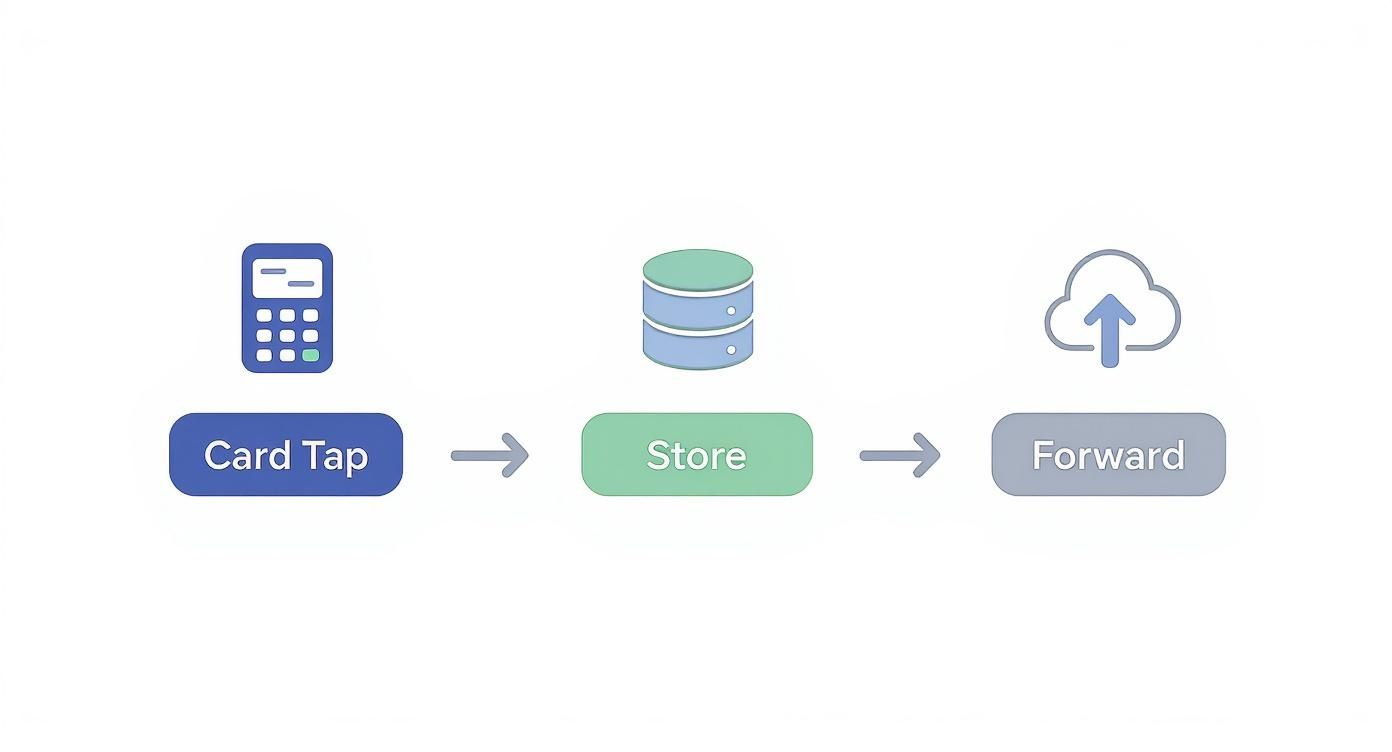

Understanding Store-and-Forward Processing

Store-and-forward is the most common form of offline credit card transaction processing.

It is primarily designed as a temporary backup solution for businesses experiencing unexpected connectivity interruptions.

Here’s how it works:

When the internet connection fails, the payment terminal stores encrypted transaction information locally instead of sending it immediately for authorization.

Once internet service returns, the system automatically forwards the stored transaction batch to the payment processor for approval.

The process involves three basic stages:

- Capturing payment data

- Securely storing transaction information

- Forwarding transactions later for authorization

Store-and-forward processing helps businesses continue operating normally during:

temporary outages, unstable Wi-Fi conditions, or short-term network interruptions.

For example, a restaurant experiencing a temporary internet outage during dinner service can continue processing customer payments without shutting down transactions completely.

However, because payments are not approved instantly, businesses temporarily assume the risk that some transactions may later be declined.

How EMV Offline Authentication Works

EMV offline authentication is more advanced than standard store-and-forward processing.

This method is designed for environments where internet connectivity may be unavailable for extended periods.

Common examples include:

- Airline purchases

- Remote transportation systems

- Mobile ticketing operations

- Outdoor event terminals

- Remote field sales environments

Unlike store-and-forward systems that simply save payment information temporarily, EMV offline authentication allows the payment terminal and the card’s EMV chip to perform security checks directly.

The chip and terminal conduct a secure cryptographic exchange without contacting the bank immediately.

This process typically includes:

- Card validation

- Cryptographic signature generation

- Risk assessment rules

- Offline approval thresholds

The EMV chip generates a unique transaction cryptogram that helps verify card authenticity locally.

This allows certain transactions to receive temporary approval even without network connectivity.

EMV offline authentication provides stronger security compared to traditional magnetic stripe processing because the chip creates dynamic encrypted transaction data that is difficult to duplicate fraudulently.

The Journey of an Offline Payment

Offline credit card transactions follow a delayed approval process rather than an instant authorization flow.

The transaction journey usually happens in two stages:

- The store phase

- The forward phase

The Store Phase

During the store phase, the payment terminal captures the customer’s card information and stores it securely within the device.

The transaction is encrypted immediately.

No communication occurs yet with the customer’s bank.

The customer receives a provisional approval, allowing the purchase to continue normally.

At this stage:

the transaction still has not officially cleared.

The payment information simply waits securely within the POS system until connectivity is restored.

The Forward Phase

Once internet access returns, the terminal automatically forwards all stored transactions to the payment processor.

The processor then routes each payment through:

card networks, payment gateways, and issuing banks for official authorization.

At that moment, the bank finally verifies:

- Available funds

- Card validity

- Fraud indicators

- Account status

- Transaction legitimacy

If approved, funds move toward settlement normally.

If declined, the business absorbs the financial loss because the customer has usually already left.

Risks and Responsibilities for Businesses

Offline payments provide operational flexibility, but they also shift financial risk directly to the merchant.

Because transactions are not verified immediately, businesses accept payments essentially on trust until the bank officially approves them later.

This creates several important risks.

Declined Transactions

The biggest risk is delayed payment rejection.

When stored transactions are finally submitted online, some cards may be declined because of:

- Insufficient funds

- Expired cards

- Frozen accounts

- Stolen cards

- Fraud blocks

At that point, recovering payment becomes extremely difficult because the customer has already left.

Chargebacks and Fraud

Offline transactions also increase chargeback risk.

Since the payment was not authorized in real time, businesses may have reduced protection during fraud disputes.

Fraudsters may intentionally target businesses operating in offline mode because delayed authorization creates additional opportunity for abuse.

Operational Liability

Merchants are responsible for maintaining secure handling of stored payment data.

Failing to protect card information properly can create:

compliance violations, legal exposure, financial penalties, and reputational damage.

Security and PCI Compliance for Offline Payments

Businesses handling offline transactions must comply with:

PCI DSS (Payment Card Industry Data Security Standard) requirements.

Even temporarily stored transaction data must remain encrypted and protected properly.

Modern POS systems use several important security technologies.

End-to-End Encryption

End-to-end encryption immediately scrambles payment information once the card is inserted, tapped, or swiped.

This prevents unauthorized parties from reading sensitive card data.

Tokenization

Tokenization replaces the actual card number with a unique substitute token.

The stored token becomes useless to attackers because it cannot recreate the original payment information.

EMV Security Protections

EMV chip cards generate dynamic cryptographic transaction codes that are much harder to counterfeit than traditional magnetic stripe cards.

This significantly reduces fraud exposure during offline processing.

Businesses should never store raw unencrypted payment information manually.

Using PCI-compliant POS systems is critical for protecting both the business and customers.

Best Practices for Managing Offline Transactions

Businesses should establish clear procedures for safely managing offline payment mode.

Set Offline Transaction Limits

Modern POS systems allow businesses to define:

- Maximum transaction values

- Total offline sales limits

- Approval thresholds

For example, a coffee shop may limit offline transactions to:

$50 per sale.

This reduces financial exposure if payments are later declined.

Train Employees Properly

Staff should understand:

- How offline mode works

- When to activate it

- What payment types are acceptable

- How to identify suspicious transactions

- How to explain the process to customers

Strong employee training reduces operational mistakes during outages.

Reconcile Transactions Quickly

As soon as internet service returns, businesses should process and review stored transactions immediately.

Quick reconciliation helps identify:

declined transactions, failed authorizations, and operational inconsistencies.

The longer transactions remain unprocessed, the higher the financial and compliance risk becomes.

Use Modern EMV-Compatible Hardware

Businesses should always use modern:

EMV-capable and PCI-compliant payment terminals.

Older magnetic stripe systems provide weaker security protections and higher fraud exposure.

Why Offline Payment Capability Matters More Than Ever

Modern commerce increasingly depends on uninterrupted payment processing.

Consumers expect businesses to accept card payments consistently regardless of internet conditions.

As businesses become more mobile and digital, offline payment capability is becoming increasingly important for:

- Restaurants

- Retail stores

- Food trucks

- Outdoor events

- Transportation systems

- Remote vendors

- Temporary sales environments

At the same time, global card payment usage continues growing rapidly.

That growth makes resilient payment infrastructure even more essential.

Businesses that cannot process payments during outages risk:

revenue loss, operational disruption, customer dissatisfaction, and reputational damage.

Offline transaction capability provides operational resilience while helping businesses continue serving customers under unpredictable conditions.

How Biyo POS Helps Businesses Handle Offline Payments

Biyo POS helps businesses manage offline credit card transactions securely through integrated cloud-based payment and POS technology.

The platform supports:

offline transaction processing, secure payment encryption, reporting tools, transaction tracking, inventory synchronization, and operational continuity during connectivity disruptions.

Biyo POS also allows businesses to configure:

offline transaction limits, approval controls, and operational safeguards to reduce financial risk.

With modern payment security features and integrated management tools, businesses can continue serving customers confidently even during temporary outages.

If you want to modernize your payment operations and improve business continuity, you can explore the platform directly through the Biyo POS signup page.

Frequently Asked Questions

What is an offline credit card transaction?

An offline credit card transaction is a payment temporarily processed without real-time internet connectivity. The transaction data is stored securely and submitted later once connectivity returns.

Are offline credit card transactions safe?

Yes, modern offline payment systems use encryption, tokenization, and EMV security technologies to protect transaction data securely.

What is the biggest risk of offline transactions?

The biggest risk is that the customer’s bank may later decline the transaction after the customer has already left the business.

Can debit cards be processed offline?

Debit cards are generally riskier in offline mode because they often require real-time PIN verification and bank authorization.

How long can offline transactions remain stored?

Most POS systems can securely store offline transactions for 24 to 72 hours depending on processor settings and terminal configuration.

How does Biyo POS help businesses with offline payments?

Biyo POS helps businesses process secure offline transactions, manage payment continuity, configure transaction limits, and maintain operational efficiency during internet outages.