So, what exactly is a payment processor? Think of it as the financial engine that handles the entire transaction journey, moving money securely from your customer’s bank account to yours. Every time a customer taps a card, inserts a chip, scans a mobile wallet, or completes an online checkout, a payment processor is working quietly behind the scenes to validate the transaction and move funds between financial institutions. Without this technology, modern commerce simply would not function.

For business owners, understanding payment processors is essential because they influence how quickly you get paid, how secure your transactions are, and how much you pay in fees. Whether you operate a restaurant, retail store, service business, or e-commerce website, your ability to accept electronic payments depends on the efficiency and reliability of your payment processor.

In today’s digital economy, electronic payments dominate consumer behavior. According to global payment industry research, digital and card-based payments account for more than 70% of consumer transactions in many developed markets. Mobile wallets, contactless payments, and online checkout systems continue to grow rapidly, making payment processors one of the most critical components of modern financial infrastructure.

This guide explores how payment processors work, what role they play in a transaction, how they differ from gateways and merchant accounts, and how businesses can choose the right processing partner.

Table of Contents

- Understanding the Role of a Payment Processor

- How a Payment Transaction Works

- Payment Processor vs Gateway vs Merchant Account

- Payment Processor Fees and Pricing Models

- How to Choose the Right Payment Processor

- Security and Compliance in Payment Processing

- The Future of Payment Processing Technology

- How Biyo Supports Businesses with Payment Processing

- FAQ

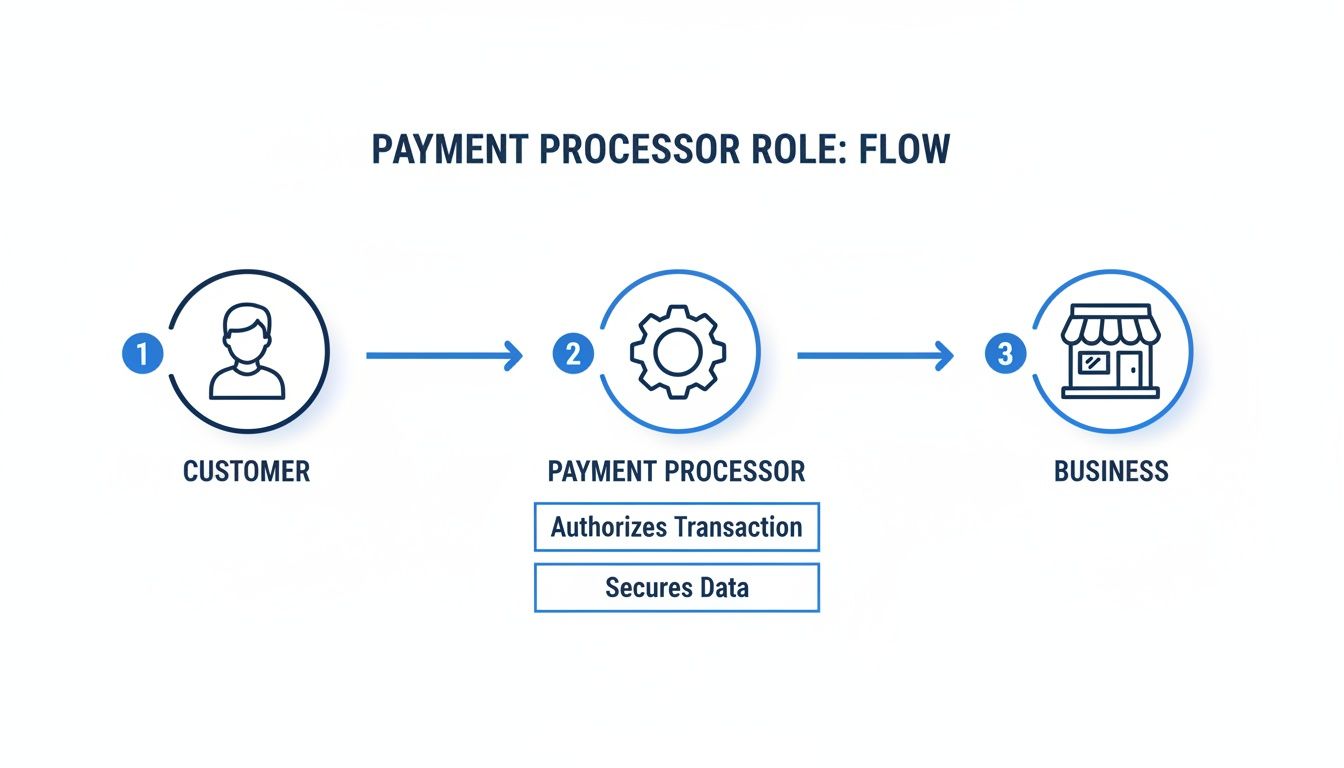

Understanding the Role of a Payment Processor

A payment processor acts as the communication bridge between your business, the customer’s bank, and the card networks that validate and route transactions. Every electronic payment passes through this infrastructure. When a customer pays using a credit card, debit card, or digital wallet, the processor securely transmits the payment request across multiple financial systems within seconds.

The role of the processor is to confirm that the payment is legitimate, that the customer has sufficient funds or credit available, and that the transaction complies with fraud detection and security requirements. If everything checks out, the processor approves the transaction and initiates the transfer of funds from the customer’s account to the merchant’s bank account.

The Core Function of a Processor

The core responsibility of a payment processor is authorization and settlement. During authorization, the processor verifies that the payment details are valid and that the funds are available. This step usually takes only a few seconds but involves multiple systems working together, including the card network and the issuing bank.

Once a transaction is approved, the processor ensures that the funds are eventually transferred to the merchant through a process known as settlement. Settlement usually happens in batches at the end of the business day, allowing processors to efficiently move thousands or even millions of transactions between banks.

Key Responsibilities in the Payment Network

Payment processors handle several important responsibilities during each transaction. They validate payment credentials, encrypt sensitive information to prevent fraud, route payment requests through card networks such as Visa or Mastercard, and communicate approval or decline responses back to the merchant’s system.

Because processors handle sensitive financial data, they operate within strict regulatory frameworks and security standards designed to protect both consumers and businesses. These safeguards ensure that every transaction is processed securely while minimizing the risk of fraud.

How a Payment Transaction Works

Although a transaction appears instantaneous to customers, a complex sequence of steps occurs behind the scenes. Each purchase triggers multiple communications between payment systems, banks, and financial networks before the payment is approved and funds are transferred.

Authorization: Verifying the Payment

The first stage of a transaction is authorization. When a customer presents their card or enters payment details online, the POS system sends the transaction data to the payment gateway. The gateway encrypts the information and forwards it to the payment processor.

The processor then routes the request to the appropriate card network, which passes it to the issuing bank. The bank evaluates the transaction by checking whether the card is valid, whether sufficient funds or credit are available, and whether the purchase appears legitimate based on fraud detection algorithms.

If the transaction meets all requirements, the bank sends an approval message back through the network to the processor and ultimately to the merchant’s POS system. The customer receives confirmation that the purchase has been approved.

Clearing and Settlement: Moving the Funds

After authorization, the transaction enters the clearing and settlement stages. During clearing, the payment processor collects approved transactions from the merchant and sends them in batches to the card networks. The networks coordinate the transfer of funds between issuing banks and acquiring banks.

Settlement occurs when the customer’s bank transfers the payment amount to the merchant’s acquiring bank. The acquiring bank then deposits the funds into the merchant account before transferring them to the business’s primary bank account. This process typically takes between one and three business days depending on the processor.

Payment Processor vs Gateway vs Merchant Account

Payment processing involves several components working together. While these terms are sometimes used interchangeably, they refer to different parts of the payment infrastructure. Understanding how they interact helps businesses better evaluate payment solutions.

What Is a Payment Gateway?

A payment gateway is the technology that captures and encrypts payment data at the point of sale or during an online checkout. It acts as the digital entry point for payment information, ensuring that sensitive card data is securely transmitted to the payment processor.

For example, when a customer enters card details on an e-commerce website, the payment gateway encrypts the data before sending it to the processor for authorization. The gateway also communicates approval or decline messages back to the merchant system.

What Is a Merchant Account?

A merchant account is a specialized bank account that temporarily holds funds from card transactions before they are deposited into the business’s primary bank account. When payments are settled, funds first enter the merchant account before being transferred to the merchant’s operating account.

This temporary holding stage allows the acquiring bank and processor to manage transaction batches, process refunds, and handle potential chargebacks before funds are finalized.

Payment Processor Fees and Pricing Models

While payment processors enable businesses to accept electronic payments, they also charge fees for their services. These fees compensate processors, card networks, and issuing banks for facilitating transactions and maintaining the payment infrastructure.

Common Pricing Models

The most transparent pricing structure used by processors is interchange-plus pricing. In this model, the merchant pays the interchange fee set by the card networks plus a small markup from the processor. This structure allows businesses to see exactly how much they are paying for each transaction.

Flat-rate pricing is another common model used by many modern payment service providers. In this structure, businesses pay a fixed percentage and per-transaction fee for every payment, regardless of card type. While this model simplifies billing, it may cost more for businesses with high transaction volumes.

Additional Fees Businesses May Encounter

In addition to transaction fees, processors may charge monthly service fees, PCI compliance fees, chargeback fees, or gateway usage fees. These charges vary depending on the processor and the services included in the merchant agreement.

Understanding these fees helps businesses accurately compare payment providers and calculate the true cost of accepting electronic payments.

How to Choose the Right Payment Processor

Choosing a payment processor is an important strategic decision because it affects transaction reliability, customer experience, and operating costs. Businesses should evaluate several factors before selecting a processing partner.

Evaluating Pricing and Transparency

One of the most important considerations when selecting a processor is pricing transparency. Businesses should request a detailed breakdown of transaction fees, monthly charges, and potential penalties before signing a contract.

Transparent pricing helps prevent unexpected costs and allows businesses to forecast payment processing expenses more accurately.

Integration with Business Systems

Another key factor is compatibility with existing business technology. Payment processors should integrate seamlessly with POS systems, accounting software, and e-commerce platforms to ensure smooth daily operations.

When payment systems integrate properly with other business tools, merchants benefit from automated reporting, accurate sales data, and simplified financial management.

Security and Compliance in Payment Processing

Because payment processors handle sensitive financial information, security is a central priority in the payment ecosystem. Processors implement advanced security technologies to protect payment data and prevent fraud.

PCI DSS Compliance

The Payment Card Industry Data Security Standard (PCI DSS) is a global security framework designed to protect cardholder data. Businesses that accept card payments must comply with these standards to maintain secure payment environments.

Payment processors help merchants meet PCI compliance requirements by implementing encryption, tokenization, and secure transaction processing infrastructure.

Fraud Detection and Prevention

Modern payment processors also use sophisticated fraud detection systems powered by machine learning and behavioral analysis. These systems monitor transactions in real time to identify suspicious activity and prevent unauthorized purchases.

By analyzing spending patterns and geographic data, fraud detection systems can flag transactions that appear inconsistent with normal customer behavior.

The Future of Payment Processing Technology

The payment processing industry continues to evolve rapidly as new technologies reshape how consumers pay for goods and services. Digital wallets, contactless cards, and biometric authentication are becoming increasingly common across global markets.

Rise of Digital Wallets

Mobile payment platforms such as Apple Pay, Google Pay, and other digital wallets are transforming the payment experience. These technologies allow customers to make secure purchases using smartphones, smartwatches, or other connected devices.

Payment processors must continually adapt to support new payment methods while maintaining strong security standards.

AI and Payment Automation

Artificial intelligence is also playing a growing role in payment processing. AI systems help detect fraud, optimize transaction routing, and analyze payment data to improve operational efficiency.

As payment technologies continue to evolve, processors will increasingly rely on automation and predictive analytics to enhance security and reduce processing costs.

How Biyo Supports Businesses with Payment Processing

Managing payments efficiently is essential for any modern business, and integrated POS technology can significantly simplify the process. Biyo POS provides businesses with a comprehensive platform that combines payment processing with powerful operational tools designed for restaurants, retail shops, and service businesses.

By integrating payment processing directly into the POS environment, Biyo allows merchants to manage transactions, track sales, monitor inventory, and analyze business performance from a single centralized system. This integration reduces operational complexity while providing real-time insights that help businesses make better decisions.

Businesses that want to streamline their payment infrastructure can explore how the platform works by scheduling a consultation through the Schedule Call option. Companies ready to begin using the system can also create an account through the Signup page to start accepting and managing payments more efficiently.

FAQ

What is the main purpose of a payment processor?

The primary purpose of a payment processor is to facilitate electronic transactions by securely transferring payment information between merchants, banks, and card networks. The processor verifies transactions, ensures funds are available, and initiates the transfer of money from the customer’s account to the merchant.

How long does payment processing take?

Authorization usually happens within seconds during a transaction. However, the full settlement process typically takes one to three business days before funds are deposited into the merchant’s bank account.

Do online businesses need a payment processor?

Yes. Online businesses rely on payment processors to handle digital transactions securely. Without a processor, e-commerce websites would not be able to accept credit card, debit card, or digital wallet payments.

Can businesses change payment processors?

Businesses can switch payment processors if they are dissatisfied with their current provider. However, they should review contract terms carefully to avoid early termination fees or other penalties before making the transition.

What industries rely on payment processors?

Nearly every industry relies on payment processors, including retail, restaurants, healthcare, hospitality, transportation, and e-commerce. Any business that accepts electronic payments requires a processor to complete transactions securely.