Zero-fee credit card processing is a pretty simple concept: it lets businesses pass their credit card transaction costs directly to the customer. This usually happens one of two ways—either by adding a small surcharge for card payments or by offering a discount to customers who pay with cash.

The end result? The merchant pays nothing to accept credit cards.

The Hidden Costs of Card Fees and a Path to Zero

If you're a business owner, you've probably come to accept credit card fees as a painful but necessary part of the deal. That small percentage taken from every single transaction might not seem like much at first, but it adds up fast. Think of it as a slow, constant leak in your revenue bucket—drip by drip, profits are quietly draining away all year long.

And this isn't just a minor expense. U.S. merchants paid an eye-watering $187.20 billion in credit card processing fees in just one year, an 8.7% jump from the year before. For most small businesses, these fees hover somewhere between 2.5% and 3.5% per transaction. That means you're losing up to $3.50 on every $100 sale right off the top.

Quantifying the Impact on Your Bottom Line

Let's break down what that actually looks like. Imagine a small retail shop that does $30,000 in credit card sales a month. At an average rate of 3%, that business is losing $900 every single month.

Over a year, that's more than $10,800 in pure profit handed straight to payment processors. That's money that could have gone toward a new marketing push, upgraded equipment, or even well-deserved employee bonuses.

This constant financial drain comes from a confusing mix of charges, but the biggest culprit is usually the interchange fee, which goes to the customer’s bank. Not only are these costs significant, but they’re also on the rise, squeezing your profit margins tighter and tighter.

The real problem is that fee growth is outpacing sales growth. This means merchants are paying higher effective rates each year, making it harder to stay profitable even as sales increase.

A Powerful Financial Strategy

This is exactly where zero-fee credit card processing comes in. It’s not some complicated gimmick; it’s a straightforward financial strategy that shifts the cost from your business to the customers who opt for the convenience of paying with a card. By doing this, you're essentially patching that leak in your revenue bucket for good.

This approach turns a major expense back into working capital. Instead of watching your profits vanish with every swipe, you can redirect those thousands of dollars back into growing your business. It's a simple shift that puts you back in control of your hard-earned money.

How Zero Fee Processing Actually Works

When you first hear "zero fee," it's natural to be a bit skeptical. Is it a gimmick? Too good to be true? In reality, it’s a straightforward financial model that all comes down to giving your customers a choice in how they pay.

Think of it like choosing your seat on an airplane. Some passengers are happy to pay a little extra for a specific seat, while others are fine with the standard, no-frills option to save a few bucks. Zero fee processing works on a similar principle: it simply passes the transaction cost to the customer who opts for the convenience of paying by credit card.

This is done through two main methods. While they feel similar in practice, they are legally distinct, and it's important to know which one you're using to stay compliant.

The Surcharging Model Explained

Surcharging is the most direct way to eliminate your processing fees. With this setup, you add a small, fixed percentage to the bill for any customer paying with a credit card. This percentage is set to match your actual processing cost, and it must be clearly listed as a separate line item on the receipt. Transparency is key.

Here’s a quick example: A customer's bill comes to $100. Your processing cost is 3%. At checkout, a $3.00 surcharge is added to their total. The customer pays $103.00, that $3.00 covers your processing fees, and you pocket the full $100.00 from your sale. Simple as that.

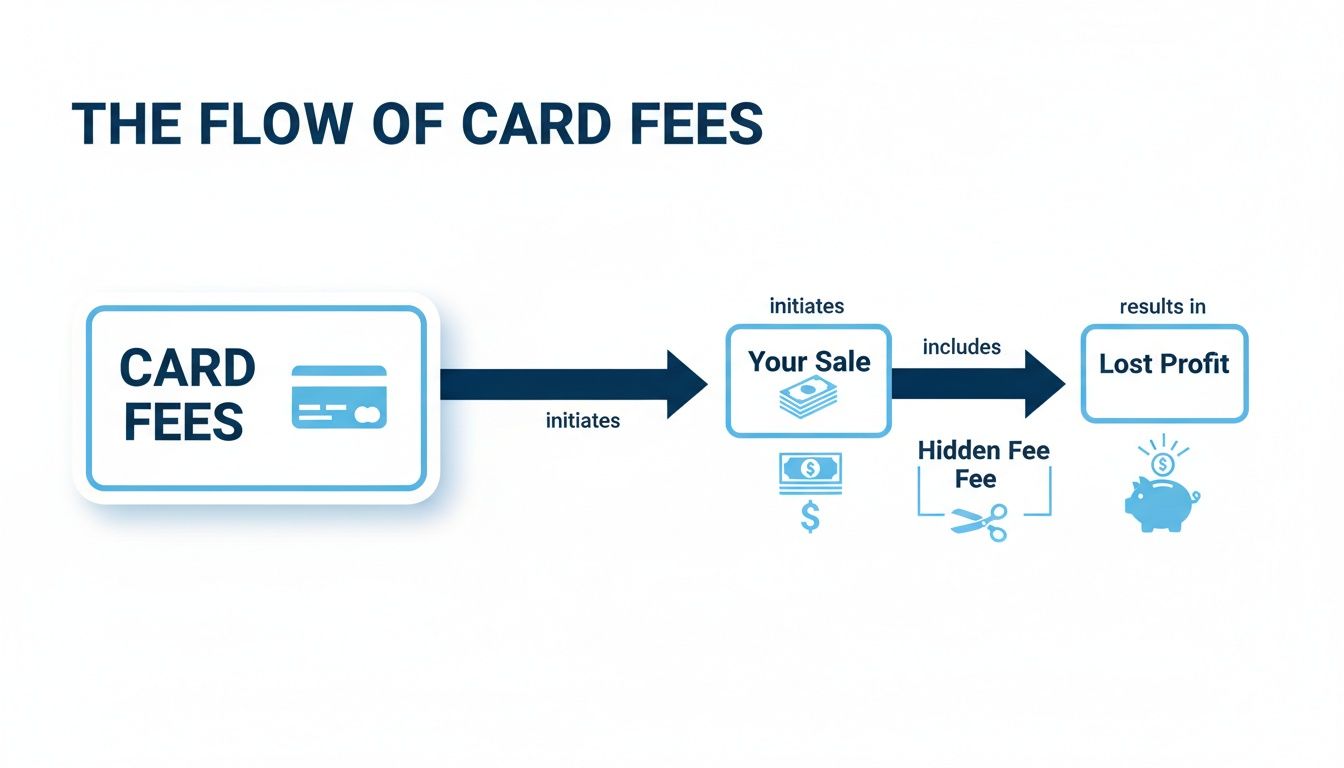

This model has become a game-changer for businesses tired of seeing their profits chipped away by swipe fees. The flowchart below really drives home how those traditional fees eat into your bottom line with every single sale.

As you can see, surcharging intercepts that hidden fee, making sure your hard-earned revenue stays in your bank account where it belongs.

Understanding the Cash Discount Program

A cash discount program gets you to the same place—no processing fees—but from a different angle. Instead of adding a fee for credit card payments, you offer a discount to customers who choose to pay with cash or debit.

Under this model, all of your advertised prices already have the cost of card processing built into them. So, you're not penalizing card users; you're rewarding cash payers.

The Bottom Line: A surcharge adds a fee for using a higher-cost payment method, while a cash discount rewards customers for using a lower-cost one. Either way, the merchant ends up paying nothing for credit card transactions.

To help you decide which approach is right for your business, let's break down the key differences side-by-side.

Surcharging vs Cash Discount Programs Explained

| Feature | Surcharging Program | Cash Discount Program |

|---|---|---|

| How It Works | Adds a fee to credit card transactions at the point of sale. | Offers a discount from the listed price for cash/debit payments. |

| Price Display | Shelf prices reflect the cash price. The fee is added at checkout. | Shelf prices reflect the card price. The discount is applied at checkout. |

| Customer Perception | Can be seen as a "penalty" for using a card. | Often viewed as a "reward" for paying with cash. |

| Legal Status | Legal in 48 U.S. states. Prohibited in Connecticut and Massachusetts. | Legal in all 50 U.S. states. |

| Receipt Requirement | The surcharge must be clearly listed as a separate line item. | The discount must be clearly shown as a separate line item. |

| Ideal For | Businesses where adding a small fee is common and accepted. | Businesses aiming to incentivize cash payments positively. |

Both models are effective tools for combating rising processing costs. With average U.S. card processing rates hovering around 2.3% and sometimes jumping as high as 3.5%, small businesses often get hit the hardest. These programs level the playing field, allowing merchants to achieve true no-cost processing with a simple, clean integration into their payment system.

Calculating the Financial Impact on Your Business

It's one thing to talk about zero-fee credit card processing in theory, but seeing the numbers on your own profit and loss statement is where it really clicks. The savings aren't just a few dollars here and there. For most businesses, this is a major financial shift that can completely reshape your budget and open up new opportunities for growth.

When you eliminate a major operating expense like this, you aren't just trimming fat—you're putting pure profit directly back into your pocket.

Let's get practical and look at what this means in real dollars. We all know processing fees hover around 3% on average, and while that sounds small, the annual total can be a real gut punch for many business owners.

Think of this recovered money as a direct boost to your bottom line. It's capital you earned but never got to keep, until now.

Real-World Savings Scenarios

To show you just how powerful this can be, let’s run the numbers for a few common business types. We'll stick with that conservative 3% processing fee to see what they'd save in a year.

-

The Neighborhood Coffee Shop: Pulling in $20,000 a month in card sales means they're losing $600 every single month to fees. That’s $7,200 a year—more than enough to buy a brand-new commercial espresso machine or run a big local marketing campaign.

-

The Busy Main Street Boutique: A retail store doing $50,000 in monthly card transactions is handing over $1,500 to their processor each month. Over a year, that's $18,000 gone. Imagine what you could do with that—hire a part-time employee or go all-in on inventory for the holiday rush.

-

The High-Volume Auto Repair Shop: A shop processing $100,000 in monthly card sales is paying a staggering $3,000 in fees every month. Annually, that’s a $36,000 hit. That kind of money could fund major equipment upgrades or even help you open a second service bay.

These aren't just made-up figures. This is real money that flows straight out of your bank account and into the hands of payment processors. Zero-fee processing simply closes that valve, turning a huge expense into a powerful asset.

Transforming Expenses into Growth Capital

The money you get back isn't just extra profit; it's an opportunity. It becomes a flexible fund you can use to make smart, strategic moves to strengthen your business.

That 3% you used to write off as a cost of doing business suddenly becomes a self-funded resource for innovation and expansion.

As you start to see the direct financial impact, it's also a good time to master small business cash flow management. After all, healthy cash flow is the lifeblood of any small business, and wiping out processing fees gives it an immediate, substantial boost. You can reinvest that capital to hire needed staff, launch a new product line, or simply build a much healthier cash cushion for whatever comes next.

Keeping It Legal and Keeping Customers Happy

Switching to a zero-fee credit card processing model can be a game-changer for your bottom line. But for it to work, you absolutely have to nail two things: staying legally compliant and communicating the change clearly to your customers. Getting this wrong isn't an option—it can lead to hefty fines, unhappy customers, and could even get your merchant account shut down.

The rules you need to follow come from a mix of state laws and the strict guidelines set by the big card networks like Visa and Mastercard. The whole idea of passing on fees gained serious traction after a major settlement with these card giants, which was expected to save U.S. businesses tens of billions by making it easier to guide customers to cheaper payment methods. Today, programs like surcharging are perfectly legal in almost every state, but you have to follow the playbook to the letter.

The Must-Follow Compliance Rules

To keep your business in the clear with both the law and the card brands, there are a few non-negotiable rules. They’re all about being upfront and fair with your customers.

- Post Clear Signs: You must have obvious signage at your entrance and at the checkout counter. This tells customers about the fee before they get to the point of paying.

- Show It on the Receipt: The fee has to be its own separate line item on the customer’s receipt. You can't just roll it into the total price of what they're buying.

- Don't Profit from Fees: The amount you add can't be more than what it actually costs you to process that specific card payment. Most states cap this at a certain percentage, but the golden rule is you can never make a profit from the fee.

Following these core rules creates a transparent system that protects both you and your customers.

"A lot of people think these programs operate in a legal gray area, but that's just not true. The rules are clearly spelled out by the card networks and state laws. The whole thing hinges on being completely transparent and following the disclosure rules."

How to Talk to Your Customers About the Change

Beyond the legal signs, the way you talk about this new policy is everything. A positive, clear message can head off any potential frustration and even build a little goodwill.

Think of it less as a penalty for using a credit card and more as a way to offer fair pricing for everyone. Explain that this model helps you avoid raising prices across the board. That way, customers who choose to pay with cash or debit aren't picking up the tab for expensive credit card reward programs. It’s all about keeping your prices competitive and delivering fair value.

Keeping up with these standards is also a big part of your business's overall security. To get a better handle on that, you can dive into our guide on the Payment Card Industry Data Security Standard (PCI DSS).

How Biyo POS Makes Zero-Fee Processing Effortless

Knowing that zero-fee processing can save you a ton of money is the easy part. Actually putting it into practice without creating a daily nightmare for your team? That’s a different story. This is precisely where having the right Point of Sale (POS) system makes all the difference. We designed Biyo POS to make switching to a zero-fee model feel completely seamless, handling everything from the math to the legal fine print automatically.

Forget about your staff fumbling with calculators or juggling separate terminals. Biyo builds zero-fee processing right into the software. This simple integration wipes out the risk of human error, guarantees every single transaction is handled correctly, and keeps your checkout lines from backing up. Think of it as your built-in compliance partner, taking all the guesswork off your plate.

Automated and Compliant Transactions

Whether you go with a surcharge program or a cash discount model, Biyo POS does the heavy lifting for you. The software is smart enough to see how a customer is paying and instantly applies the right adjustment. No manual entry, no mistakes—just accuracy and consistency with every sale.

The system also ensures you’re being completely transparent by adding the required line-item details to every receipt, which is a non-negotiable rule set by card brands like Visa and Mastercard. Biyo handles this automatically, so you can spend your time running your business instead of trying to memorize a rulebook.

By automating compliance, Biyo POS removes the single biggest hurdle for businesses wanting to adopt a zero-fee model. It turns a complex legal process into a simple, background function of your daily operations.

Streamlining Your Payment Workflow

An all-in-one system like Biyo isn't just about saving money; it’s a massive boost to your day-to-day efficiency. Your team doesn’t need any special training on how to calculate fees or follow compliance steps because the POS guides them through it all. This simplicity means fewer mistakes and a much smoother, more professional checkout experience for your customers.

For any business owner serious about optimizing their payment setup, getting the fundamentals right is everything. You can dive deeper into how to best process credit card payments in our detailed guide. Biyo essentially bundles all those best practices into one intuitive platform.

Ultimately, Biyo POS is your tool for both saving money and running a tighter ship. It lets your business capture the full financial benefits of zero fee credit card processing without adding any complexity to your workflow. It's a smart move for both your efficiency and your bottom line.

Is Zero-Fee Processing the Right Move for You?

The idea of wiping out credit card processing fees sounds fantastic, but let's be real—it's not a magic bullet for every business. Before you jump in, you need to take an honest look at your operations, your customers, and where you stand in the market. For some, it's a game-changing financial strategy. For others, it can introduce friction you just don't need.

The sweet spot for a zero-fee program is often with businesses that handle a ton of transactions or run on razor-thin margins. Think about a bustling coffee shop, a busy convenience store, or any place where saving 3% on countless small purchases snowballs into huge savings by the end of the year. That's where this model really shines.

Evaluating Your Business Model

On the flip side, this approach might not sit well in luxury markets. If you're running a high-end boutique or offering premium services, your entire brand is built on a seamless, top-tier customer experience. Tacking on a service fee at the last second, no matter how small, can cheapen that feeling of exclusivity and might even chip away at customer loyalty.

You also have to consider what your direct competitors are doing. If everyone else on your block absorbs card fees as a cost of business, you don't want to be the one standout that passes them along. It’s a delicate balance; you have to weigh the immediate cash savings against the potential ripple effects on how customers see you and where you fit in the local market.

Deciding to switch isn't just a numbers game; it's a strategic one. You're balancing direct cost savings against the long-term health of your customer relationships and brand perception.

A Checklist to Guide Your Decision

So, how do you figure out if zero-fee processing is a smart move for you? It helps to put your business under the microscope and ask some tough questions. This little self-audit can give you the clarity you need to make the right call.

-

What are my average profit margins? If you're working with slim margins, getting rid of a 3% fee can instantly and significantly fatten up your bottom line.

-

Who is my typical customer? Are they budget-conscious folks who would jump at the chance to save a little by paying cash? Or are they all about convenience and likely to be annoyed by an extra fee on their card?

-

What is the competitive landscape like? Take a peek at what the other shops in your area are doing. If passing on fees is already the norm, you probably won't get much pushback.

-

How important is a premium experience? If your brand screams luxury and effortless service, eating the processing fees might just be part of the cost of maintaining that polished image.

To help you sort through these factors, we’ve put together a simple table. It lays out the ideal scenarios for adopting a zero-fee model against the potential roadblocks you might encounter.

Should Your Business Adopt Zero Fee Processing?

A checklist to help business owners evaluate if a zero fee model is a strategic fit for their operations and customer base.

| Consideration | Ideal Scenario for Zero Fee | Potential Challenges |

|---|---|---|

| Profit Margins | Your margins are tight (e.g., retail, QSR), and eliminating a 2-3% fee provides a critical boost. | Your business has high margins and can easily absorb fees as a standard operational cost. |

| Customer Base | Your customers are price-sensitive and appreciate having a lower-cost cash or debit option. | Your clientele values convenience above all and may perceive a card surcharge as poor service. |

| Competitive Environment | Your direct competitors already use a similar surcharge or cash discount model. | You are the only business in your local market passing fees to customers, creating a disadvantage. |

| Brand Identity | Your brand is focused on value, affordability, and providing clear cost options to customers. | Your brand is built on luxury, exclusivity, and a frictionless, all-inclusive experience. |

| Transaction Size | You have a high volume of small to medium-sized transactions where the fee is minimal per customer. | You process large, infrequent transactions where the added fee becomes very noticeable and potentially a deal-breaker. |

Ultimately, looking at these points will give you a much clearer picture. The goal is to find a solution that not only helps your finances but also aligns perfectly with the business you’ve worked so hard to build.

Still Have Questions About Zero Fee Processing?

Even after getting the rundown on how zero-fee processing works, it's natural to have a few more questions pop up. Let's tackle some of the most common things business owners ask before they decide to make the change.

Is Passing on Credit Card Fees Actually Legal?

Yes, absolutely. For a long time, this was a gray area, but thanks to some major legal shifts and new state laws, it's now perfectly legal for merchants in 48 states to pass these costs to customers who choose to pay by card.

The trick is doing it the right way. You have to play by the rules set by the card brands (like Visa and Mastercard) and follow any local state laws. This means being upfront with your customers—putting up signs and clearly listing the fee on their receipts. As long as you're transparent, you're on solid legal ground.

How Will My Customers React?

This is probably the number one worry for any business owner, but in my experience, it's rarely the big deal people expect it to be. It all comes down to how you communicate it.

When you explain that this small fee helps you avoid raising prices across the board for everyone, most people get it. They understand you're just trying to cover a direct cost. Think about it: customers in places like small retail shops or quick-service restaurants are already used to seeing discounts for paying with cash. You're just framing it a different way, and that simple choice goes a long way in keeping them happy.

The Bottom Line: Most customers have no problem paying a small amount for the convenience of using their card. As long as you're clear and honest about it from the start, you’ll find that any negative feedback is incredibly rare.

What’s Involved in Switching Over?

Making the move from a traditional processing model to a zero-fee credit card processing program is much easier than you’d think, especially when you have the right partner. It really just breaks down into a few simple steps:

- Find a Specialist: You'll want to team up with a payment processor who lives and breathes zero-fee solutions. They’ll ensure everything is set up to meet all the card brand and state rules.

- Get Your POS Ready: Your provider will handle the software side, integrating it with your POS so that the fees are calculated and printed on receipts automatically.

- Post the Signs: They’ll also give you the required signs to post at your entrance and at the checkout counter, letting customers know about the policy before they pay.

With a modern POS system, all the heavy lifting is done for you. The transition feels smooth and doesn't throw a wrench into your daily operations.

Ready to stop watching processing fees eat into your profits and put that money back where it belongs? Biyo POS has a fully compliant, automated zero-fee solution built right in, making the switch a total breeze. See exactly how much you could be saving by visiting the Biyo POS website and starting your free trial today.