Accepting credit cards is no longer optional for modern businesses. Whether you operate a retail store, restaurant, service company, or online shop, customers expect fast and convenient payment options. To accept credit card payments, businesses typically need two key components: a merchant account where funds are deposited and a payment processor that securely handles the transaction between the customer’s bank and your business.

With the right setup, businesses can accept payments in-store, online, or on mobile devices. This guide explains how credit card processing works, the different pricing models available, and how to choose the right hardware and software for your business.

Why Your Business Needs to Accept Credit Cards Today

Consumer payment behavior has changed dramatically in recent years. Digital payments and card transactions now dominate both retail and online commerce. Businesses that fail to accept credit cards risk losing customers who expect quick, secure, and convenient payment options.

Accepting card payments improves customer experience while also increasing average order values. Studies consistently show that customers tend to spend more when paying with cards compared to cash.

In many developed economies, the majority of merchants now accept credit cards. Industry data suggests that by 2025, more than 90% of businesses in the United States accept card payments, making it the standard method of payment for modern commerce.

Understanding the Modern Payment Landscape

Every credit card transaction involves several entities working together to authorize and process payments. The three essential components include:

- Merchant Account: A specialized bank account used to temporarily hold funds from card payments before they are transferred to your business bank account.

- Payment Processor: The technology provider that securely communicates between your business, the customer’s bank, and the credit card networks.

- Payment Hardware or Software: The tools used to capture payment information, such as POS terminals, mobile card readers, or online payment gateways.

When a customer taps, inserts, or enters their card details, the payment processor verifies the transaction with the issuing bank. Once approved, the funds are transferred to the merchant account and later deposited into the business bank account.

The Real Cost of Being Cash-Only

Choosing not to accept card payments can significantly limit business growth. Cash-only businesses often lose customers who do not carry physical currency or prefer digital payment methods.

Card acceptance not only improves convenience but also builds trust with customers. Businesses that accept digital payments are often perceived as more professional and reliable.

Businesses that introduce card payments frequently report increased transaction frequency and higher average purchase amounts, largely due to improved customer convenience.

Finding the Right Payment Processing Partner

Businesses typically choose between two payment processing models: traditional merchant account setups or modern all-in-one payment platforms.

The Traditional Route: Merchant Account and Payment Gateway

The traditional approach involves using a dedicated merchant account combined with a payment gateway.

This model allows businesses to select individual providers for different payment services, which can provide more flexibility and lower processing costs for high-volume merchants.

Key advantages include:

- Lower transaction fees for high sales volumes

- Greater customization and integration options

- More control over payment infrastructure

This approach is common for large e-commerce businesses and enterprises processing thousands of transactions each month.

The Modern Alternative: All-in-One Payment Solutions

All-in-one platforms—often called Payment Service Providers (PSPs)—bundle the merchant account, gateway, and payment processing into one simple platform.

This setup is ideal for small businesses, startups, and service providers that want fast setup and simplified pricing.

Advantages include:

- Quick account approval and onboarding

- Simple flat-rate pricing

- Integrated hardware and software solutions

Businesses such as cafes, mobile vendors, and small retail shops often benefit most from these simplified solutions.

Understanding the True Cost of Accepting Credit Cards

Every credit card transaction includes processing fees. These fees compensate banks, payment networks, and processors for authorizing and transferring payments.

Typical processing costs range from 1.5% to 3.5% per transaction depending on the pricing model and card type.

Main Payment Processing Pricing Models

Flat-Rate Pricing

Flat-rate pricing charges the same fee for every transaction, such as 2.9% + $0.30.

This model is simple and predictable, making it ideal for small businesses or companies with low transaction volume.

Tiered Pricing

Tiered pricing groups credit cards into categories such as qualified, mid-qualified, and non-qualified. Each tier carries different fees.

This model can sometimes lead to higher costs because processors determine how transactions are categorized.

Interchange-Plus Pricing

Interchange-plus pricing separates the wholesale interchange fee charged by card networks from the processor’s markup.

This model offers the most transparency and is often the most cost-effective option for high-volume businesses.

Additional Fees to Watch For

Beyond transaction fees, merchants may encounter additional charges such as:

- Monthly account fees

- PCI compliance fees

- Chargeback penalties

- Payment terminal hardware costs

- Early contract termination fees

Before choosing a payment processor, always request a complete fee schedule to avoid unexpected costs.

Choosing Your Payment Hardware and Software

The payment hardware and software you choose should align with how your business operates and where transactions occur.

Tools for In-Person Sales

- Countertop Payment Terminals: Traditional card machines commonly used in retail stores.

- POS Systems: Integrated systems that combine payments, inventory management, and sales analytics.

- Mobile Card Readers: Portable devices that allow businesses to accept payments using smartphones or tablets.

Solutions for Online Payments

Businesses selling online require digital payment solutions rather than physical hardware.

- Payment Gateways: Secure technology that connects websites to payment processors.

- E-commerce integrations: Plugins for platforms like Shopify, WooCommerce, or BigCommerce.

- Virtual Terminals: Web-based tools that allow manual card entry for phone or invoice payments.

Essential Payment Features

Modern payment systems should support:

- EMV chip card processing

- Contactless payments (tap-to-pay)

- Mobile wallets such as Apple Pay and Google Pay

- Fraud detection tools

- Tokenization for secure data storage

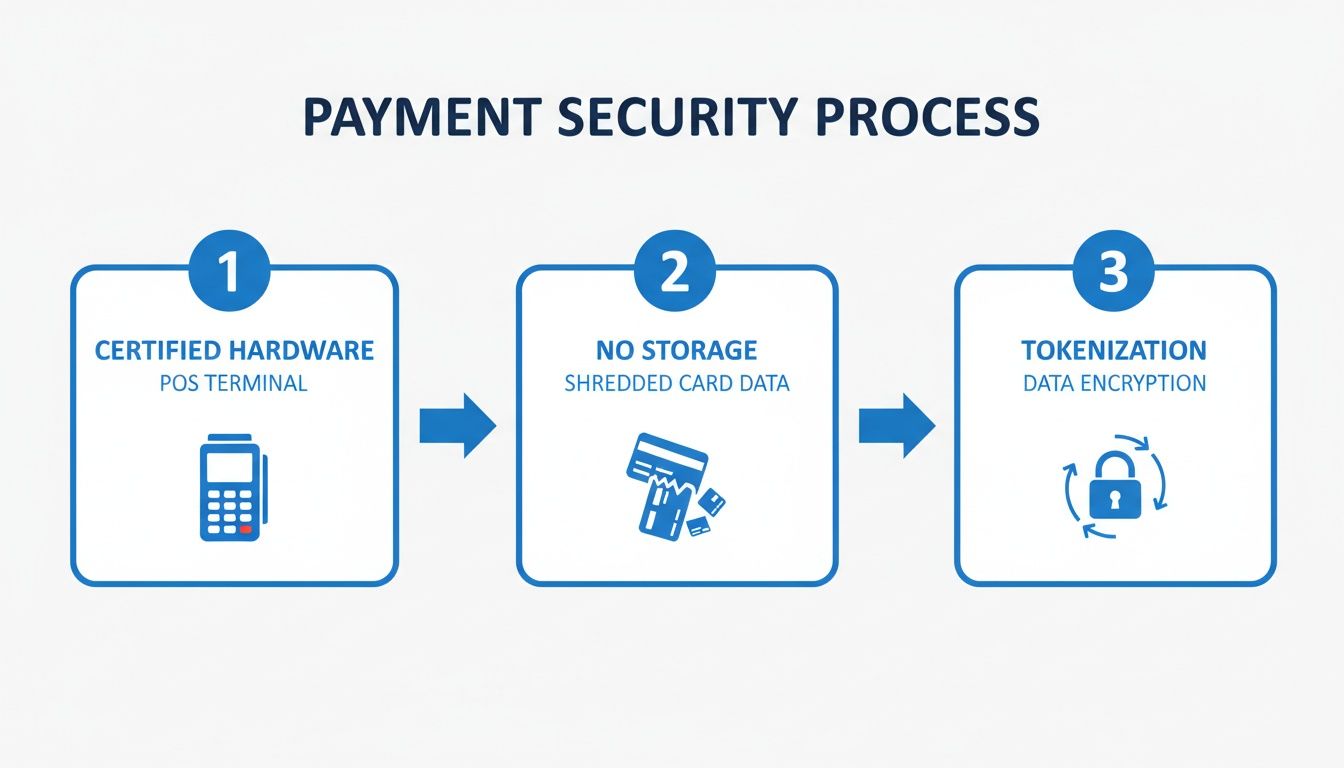

Mastering Payment Security and PCI Compliance

Handling credit card payments requires strict security standards to protect customer data. These standards are defined by the Payment Card Industry Data Security Standard (PCI DSS).

PCI compliance ensures that businesses follow proper security procedures when processing or transmitting cardholder data.

Businesses can simplify compliance by:

- Using PCI-certified payment hardware and software

- Avoiding storage of card numbers

- Implementing encrypted payment systems

Modern payment technologies also use tokenization, which replaces card numbers with encrypted tokens. This protects sensitive data even if a system breach occurs.

Most small businesses complete an annual PCI Self-Assessment Questionnaire (SAQ) to verify compliance.

Your Final Checklist Before Accepting Credit Cards

Before launching your new payment system, perform a few final checks to ensure everything works properly.

- Run a test transaction and refund to confirm processing works

- Verify funds deposit correctly into your merchant account

- Train employees on processing payments and issuing refunds

- Prepare staff for handling declined transactions professionally

Promote Your New Payment Options

Once your system is live, inform customers that you accept credit cards. Display card network logos at your store entrance or website checkout page to signal convenient payment options.

Visible acceptance badges help build trust and encourage customers to complete purchases.

How Biyo POS Helps Businesses Accept Credit Cards

Biyo POS provides an all-in-one payment and business management system designed for modern businesses. The platform combines payment processing, inventory management, reporting, and customer management into a single easy-to-use solution.

With Biyo POS, businesses can:

- Accept credit cards, mobile wallets, and contactless payments

- Manage in-store and online transactions

- Track sales performance and analytics

- Maintain secure PCI-compliant payment processing

By integrating payments with powerful business tools, Biyo POS helps businesses streamline operations while delivering a smooth checkout experience for customers.

Frequently Asked Questions

Do I need to accept every type of credit card?

No. Most businesses only need to accept major networks such as Visa, Mastercard, and American Express to cover the majority of transactions.

Can businesses charge customers credit card processing fees?

Some regions allow businesses to apply surcharges for credit card payments, but rules vary by state or country. Debit card transactions typically cannot be surcharged.

Can businesses accept international credit cards?

Yes. Most payment processors support international cards, although currency conversion and cross-border processing fees may apply.

How long does it take to receive credit card payments?

Most processors deposit funds into your business bank account within one to three business days after the transaction is processed.