If you've ever looked at your monthly sales and wondered why the total deposit doesn't quite match your revenue, you've met merchant fees. These are the costs every business pays to accept credit and debit card payments, and they are simply part of the deal for processing digital transactions securely.

Typically, these fees add up to anywhere between 1.5% to 3.5% of each sale.

The Real Cost of Accepting Digital Payments

Think of merchant fees as the cost of admission to the modern marketplace. Your customers expect the convenience of paying with a card, and these fees are what make that quick, secure tap, swipe, or click possible.

Every time a customer pays, a rapid-fire chain of events kicks off behind the scenes. This intricate process involves a handful of different players, and each one takes a tiny slice of the transaction for the role they play.

The Key Players in Every Transaction

So, who exactly is getting a piece of the pie? Understanding this is the key to demystifying your processing statement. Four main parties are involved in every card payment:

- The Issuing Bank: This is your customer's bank (think Chase, Citi, or your local credit union) that issued their card. They take the biggest cut to cover the risks of fraud and to help fund those popular rewards programs.

- The Acquiring Bank: This is your business bank, the one that provides your merchant account and deposits the funds from card sales into your account.

- The Card Network: These are the household names like Visa, Mastercard, and American Express. They act as the traffic controllers, setting the rules of the road and routing the transaction data between all the other players.

- The Payment Processor: This is the tech partner that connects your point-of-sale system to the card networks and banks, essentially facilitating the entire transaction from start to finish.

A "merchant fee" isn't a single charge. It's actually a bundle of smaller costs collected by each of these players. Getting a handle on this is the first step toward managing your expenses and protecting your profit margins.

This financial ecosystem is what ensures payments are authorized in seconds, funds are transferred safely, and any disputes are handled properly. As technology moves forward, some businesses are even exploring a new era of crypto gateway payment solutions to work alongside traditional methods.

In the next sections, we’ll break down exactly what makes up these bundled fees.

Breaking Down the Three Core Merchant Fees

If you've ever looked at your payment processing statement and just seen one blended rate, it's easy to miss what's really going on behind the scenes. That single percentage is actually a combination of three separate fees, each going to a different party.

Getting a grip on these components is the first real step toward taking control of your costs. Think of it like a pizza delivery. The final price you pay isn't just for the pizza; it's a mix of the pizza itself, the box it comes in, and the delivery driver's fee. Merchant fees are built the same way.

H3: Interchange Fees: The Main Ingredient

First and foremost is the interchange fee. In our pizza analogy, this is the cost of the pizza itself—the dough, cheese, and toppings. It’s the single biggest chunk of the cost, making up a massive 70-90% of your total processing fees.

This fee is non-negotiable. It’s set by the card networks (think Visa and Mastercard) and paid directly to the bank that issued your customer's credit or debit card. Why? It covers the bank's risk of fraud and helps fund those popular customer rewards programs, like airline miles and cash-back offers.

Interchange rates aren't a flat number. They change constantly based on a whole host of factors, including:

- Card Type: A high-end rewards credit card costs you more to accept than a basic debit card.

- How You Process: An online or keyed-in sale ("card-not-present") is seen as riskier, so it carries a higher rate than a chip-and-PIN transaction.

- Your Industry: Different business types (restaurants, retail, services) have unique risk profiles that influence their rates.

H3: Assessment Fees: The Cost of the Box

Next, we have assessment fees. Sticking with our analogy, this is the pizza box. It’s a small, non-negotiable cost, but you can’t get the pizza without it.

These fees go straight to the card brands themselves—Visa, Mastercard, Discover, and American Express. It’s their charge for building and maintaining the massive, secure global networks that let you get paid in seconds. You're essentially paying for the privilege of using their brand and payment rails.

Assessment fees are a much smaller slice of the pie, usually hovering around 0.13% to 0.15% of the transaction. While they look tiny on paper, they're added to every single card transaction you run.

H3: Processor Markup: The Delivery Charge

Finally, there’s the processor markup. This is the delivery fee. It’s what your payment processor—the company you partner with for your merchant services—charges for getting the payment from your customer's bank to yours.

This is the only part of the merchant fee you can actually negotiate. The markup covers your processor's own costs, like customer support, technology, and, of course, their profit. The structure of this fee depends entirely on your pricing model, which we'll dive into later.

To give you a clearer picture of how these three fees come together, here’s a simple breakdown.

Breakdown of a Typical Merchant Fee

This table shows how a single transaction fee is split among the key players, outlining the purpose and typical cost of each component.

| Fee Component | Who It Goes To | Purpose | Typical Percentage Range |

|---|---|---|---|

| Interchange Fee | The customer's card-issuing bank | Covers transaction risk and funds customer rewards programs | 1.2% – 2.5%+ (highly variable) |

| Assessment Fee | The card brand (Visa, Mastercard, etc.) | Pays for operating and maintaining the payment network | 0.13% – 0.15% |

| Processor Markup | Your payment processor | Covers service, support, technology, and profit | 0.20% – 1.00%+ (negotiable) |

When you put it all together, this combined fee—often called the Merchant Discount Rate (MDR)—typically lands somewhere between 1.5% and 3% for most businesses. For context, U.S. interchange fees average 1.8% for credit cards but are much lower for debit cards, at just 0.3%. Understanding these details is the key to unlocking real savings.

What Else Is Lurking on Your Statement?

Once you get past the big three—interchange, assessments, and markup—you'll find a whole list of other charges on your monthly statement. These are the flat-rate and incidental fees that often fly under the radar but can seriously inflate your total processing cost. Knowing what they are is the only way to get a real handle on what you're paying.

Most of these fees cover things like account maintenance, security requirements, and the cost of dealing with customer disputes. Some are unavoidable, but many are negotiable or can be eliminated by choosing the right processor. Before you can even think about reducing these costs, you have to know where your money is going. The first step is to effectively track all business expenses for a complete picture.

Monthly and Annual Fees

These are the fixed costs you pay just to keep your merchant account open. Think of them as a subscription fee. Processors often give them official-sounding names, but they're really just service charges that go straight to their bottom line.

- Monthly Account Fee: A standard charge for basic services like statement prep, account upkeep, and customer service access. You'll typically see this run from $10 to $40 per month.

- Statement Fee: Some processors will tack on a separate fee just to mail or email you a statement, which can feel like a double-dip if you're already paying an account fee.

- Annual Fee: This one is less common, but some providers will charge a yearly fee for account maintenance.

Good news: these fees are almost entirely pure profit for the processor. That means they are highly negotiable, especially for businesses with solid sales volume.

PCI Compliance and Non-Compliance Fees

The Payment Card Industry Data Security Standard (PCI DSS) isn't optional—it's a mandatory set of security rules to protect customer card data. If you take cards, you have to comply.

Processors will usually charge a PCI compliance fee, which they claim covers their services to help you stay compliant. This fee is often $90 to $120 per year. The real sting, however, comes if you fall out of compliance.

If you fail to complete your annual PCI validation, get ready for a PCI non-compliance fee. This is a penalty, plain and simple, and it can be costly—often $20 to $50 per month until you fix the issue.

This fee is a powerful motivator to keep your security practices up to date. A data breach could be catastrophic for a small business, so it's a rule you don't want to ignore.

Chargeback and Retrieval Fees

A chargeback is what happens when a customer disputes a charge directly with their bank, and the bank yanks the money back from your account. Not only do you lose the sale, but you also get hit with a penalty.

For every single chargeback filed—whether you win the dispute or not—your processor will charge you a chargeback fee. This typically costs between $15 and $30 per incident.

Sometimes, before a full chargeback, a bank will issue a "retrieval request" to get more info on a transaction. Even for this simple inquiry, you might get charged a retrieval fee, usually around $5 to $15.

Gateway and Incidental Fees

If you sell online, you’ll likely see a payment gateway fee. This is a monthly charge for the technology that securely links your website's shopping cart to the payment network.

And there are plenty of other small-fry fees that can pop up:

- Batch Fees: A small, daily fee for settling your batch of transactions.

- Early Termination Fees (ETFs): A massive penalty charged if you try to leave your contract before it expires. This is a big red flag to watch for.

How Different Pricing Models Impact Your Final Bill

So, we've unpacked the individual fees—interchange, assessments, and the processor's cut. But how do these all get bundled together on your monthly statement? Payment processors don't just pass along the raw costs; they package them into different pricing models, and the model you’re on directly dictates what you actually pay on every single sale.

This is where things get interesting. The same $100 transaction can cost your business wildly different amounts depending on the pricing structure. It all comes down to how the processor applies their markup—that one negotiable piece of the puzzle. Let’s walk through the three most common models you’ll encounter, using that $100 sale as our example.

The Flat-Rate Pricing Model

This is the simplest kid on the block, made famous by companies like Square and Stripe. With flat-rate pricing, you pay one predictable percentage plus a small fixed fee for every transaction. It doesn't matter if it's a debit card, a fancy rewards card, or a corporate card—the rate stays the same.

A typical flat rate you might see is 2.9% + $0.30 per transaction.

- Calculation on a $100 Sale: ($100 x 2.9%) + $0.30 = $2.90 + $0.30

- Total Fee: $3.20

The biggest win here is predictability. Your bill is dead simple to read, and you always know what to expect. The trade-off? You often overpay on low-cost transactions, like debit cards, where the true interchange cost is far lower than your flat rate. That simplicity comes at a premium.

The Tiered Pricing Model

Next up is the tiered model, which adds a layer of complexity. Processors take the hundreds of different interchange rates and lump them into three main buckets: Qualified, Mid-Qualified, and Non-Qualified. They get to decide which transactions fall into which tier.

A standard debit card swiped at your counter? That will probably get the best "Qualified" rate. But a high-rewards credit card keyed in manually for an online order? That’s almost certainly landing in the expensive "Non-Qualified" tier.

The real frustration with tiered pricing is its complete lack of transparency. The processor holds all the cards, controlling which transactions get downgraded to a pricier tier. This often leads to confusing statements and unexpected cost spikes.

The Interchange-Plus Pricing Model

Also known as "cost-plus," interchange-plus pricing is by far the most transparent model out there. It works by passing the true, wholesale interchange and assessment fees directly through to you. Then, the processor adds their pre-negotiated, fixed markup on top. No buckets, no guesswork.

Let's say the real interchange fee for our transaction is 1.51% + $0.10, the card network assessment is 0.14%, and your processor's markup is a fixed 0.25% + $0.10.

- Interchange Fee: ($100 x 1.51%) + $0.10 = $1.61

- Assessment Fee: $100 x 0.14% = $0.14

- Processor Markup: ($100 x 0.25%) + $0.10 = $0.35

- Total Fee: $1.61 + $0.14 + $0.35 = $2.10

Look at that. On the exact same $100 sale, the interchange-plus model saved you over a dollar compared to the flat-rate example. While the statements are more detailed, this model guarantees you get the lowest possible rate for each card type and you know exactly how much your processor is making.

Pricing Models at a Glance

For most businesses with any significant sales volume, the transparency and cost savings of an interchange-plus model make it the clear winner. The key is knowing how to read your statements and what to ask for when negotiating with a provider.

Of course, these per-transaction models are only part of the story. You also need to keep an eye out for all the other incidental fees that can pop up on your monthly statement.

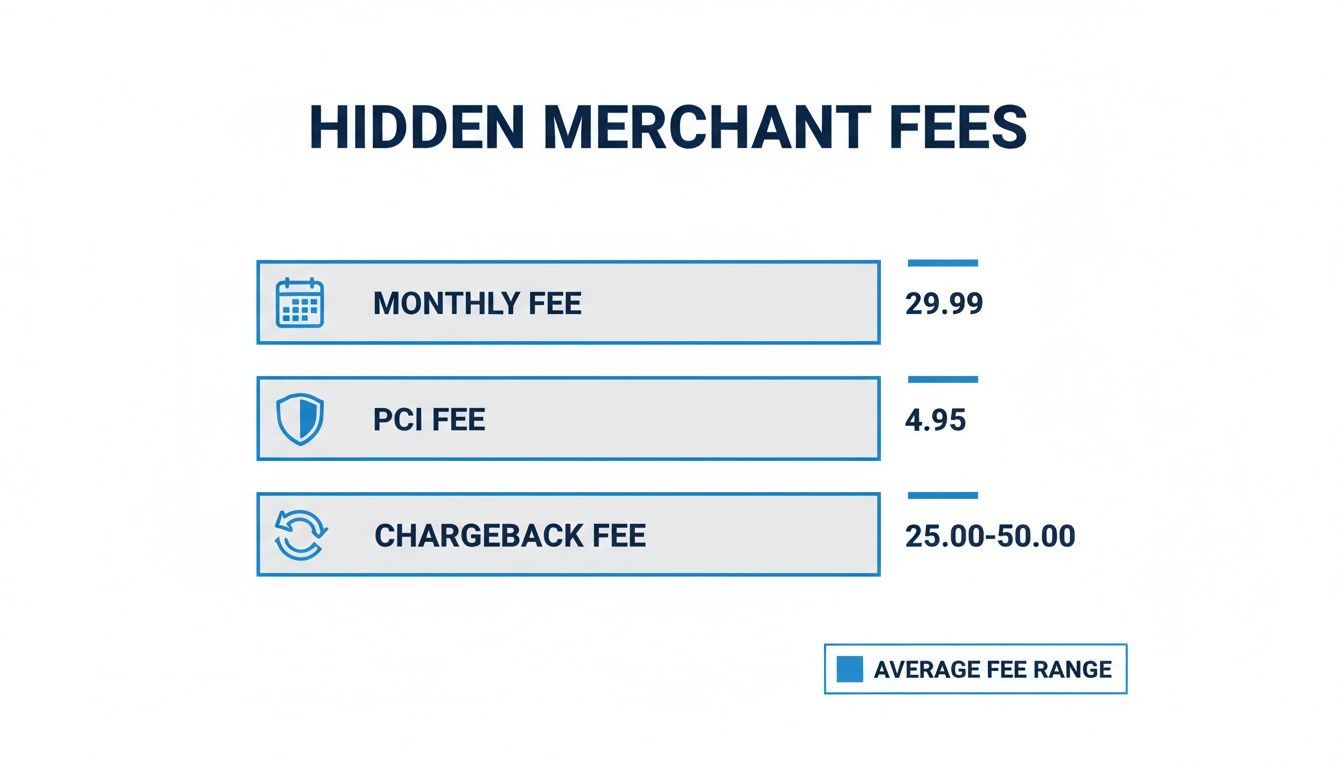

This infographic breaks down some of the most common "hidden" fees that can quietly inflate your processing bill.

As you can see, things like fixed monthly fees, security compliance charges, and dispute penalties can all add up, hitting your bottom line completely separately from your transaction rates.

Actionable Strategies to Lower Your Merchant Fees

Alright, so you’ve got a handle on the what and why of merchant fees. That's half the battle. Now comes the fun part: taking action to keep more of your hard-earned cash.

This isn’t about just finding the cheapest rate and calling it a day. It’s about building smart habits and using the right tools to continuously chip away at those processing costs. A proactive approach here can make a real difference to your bottom line.

Go Straight to the Source: Negotiate Your Processor's Markup

Here's the inside scoop: the only part of your fee structure with any real wiggle room is the processor markup. Everything else—interchange and assessments—is set by the card networks and is non-negotiable. But that markup? That's your processor's profit, and you can almost always negotiate it.

Before you even think about calling them, get your ducks in a row. Pull your last few months of processing statements and find your total sales volume, your average transaction size, and your "effective rate" (total fees divided by total sales). When you can walk into a conversation with solid numbers, you have real leverage to ask for a better deal or to confidently shop around.

In the U.S., these fees are a serious cost of doing business. Most merchants are paying somewhere between 2.5% and 3.5% on every single transaction. That's $2.50 to $3.50 vanishing from every $100 sale. For smaller businesses, it can creep even higher, sometimes topping 4.0% once all the little incidental fees are added up.

Insist on Interchange-Plus Pricing

If you make one change, let it be this: switch to an Interchange-Plus pricing model. It's the most transparent and, for most businesses, the most cost-effective way to process payments.

Instead of bundling all the costs into confusing tiers, Interchange-Plus passes the wholesale interchange and assessment fees directly to you. Then, your processor adds their markup as a separate, clearly defined percentage and per-transaction fee. No more guesswork.

When you're talking to providers, ask for an Interchange-Plus quote right out of the gate. If they hesitate or try to steer you toward a tiered or flat-rate plan, that’s a massive red flag. It often means their business model relies on hiding fees in complex pricing structures.

Key Takeaway: With Interchange-Plus, you always get the benefit of the lower wholesale interchange rates, especially on things like debit card transactions. This transparency is the key to actually controlling your costs over the long haul.

Sharpen Your Daily Operations

Believe it or not, how you handle transactions day-to-day can directly impact the interchange rates you pay. The card networks reward merchants who submit more detailed, lower-risk transaction data.

Here’s how you can make sure you're getting the best possible rates on every sale:

- Settle Your Batch Every Day: Don't let your transactions sit overnight. Settling your terminal or gateway at the end of each business day is crucial. If you wait more than 24 hours, the card networks can "downgrade" your transactions, automatically bumping them into a more expensive interchange category.

- Use Address Verification (AVS): For any sale where the card isn't physically present (online, over the phone), use an Address Verification System. Simply confirming the customer's billing zip code helps prove the transaction is legitimate, reducing your risk and helping you qualify for better rates.

- Provide Level 2 and Level 3 Data: This one is huge for B2B and B2G businesses. By submitting extra details like a PO number or sales tax amount, you can qualify for significantly lower interchange rates on corporate and government cards. Many modern POS systems can automate this for you.

Clamp Down on Card-Not-Present Fraud

Online sales and phone orders are fantastic for business, but they're also where most fraud happens. These "Card-Not-Present" (CNP) transactions naturally come with higher processing fees because the risk is greater.

By investing in simple anti-fraud tools, you not only protect yourself from costly chargebacks but also signal to processors that you're a lower-risk merchant. Activating security features like CVV verification (the three or four-digit code on the back of the card) and 3D Secure (like Verified by Visa or Mastercard SecureCode) adds a critical layer of authentication that can deter fraudsters and potentially lower your fees.

Nudge Customers Toward Cheaper Payment Options

Every payment method carries a different cost. A premium, points-heavy rewards card costs you far more to accept than a standard debit card. While you never want to create friction at checkout, you can subtly encourage more cost-effective payment types.

- Debit is Your Friend: Debit card transactions have much lower interchange fees.

- Consider ACH for Big Invoices: For large B2B payments or recurring subscriptions, an ACH bank transfer is an incredibly low-cost alternative to a credit card.

Simply making customers aware that you accept these methods can be enough to shift some volume away from high-cost credit cards, putting more money back in your pocket.

Picking the right payment processor is one of the most critical financial moves you'll make for your business. It's not about chasing the lowest rate you see in an ad; it's about finding a genuine partner who understands your business and helps protect your profits for the long haul.

That flashy, rock-bottom percentage you see advertised? It almost never tells the full story. The true cost of taking payments is a messy combination of transaction rates, monthly charges, and a whole slew of incidental fees. If you choose a partner based on one enticing number, you could find yourself locked into a costly contract full of nasty surprises on your monthly statement.

Demand Clear, Honest Pricing

The absolute best way to make sure you're getting a fair shake is to insist on an Interchange-Plus pricing model. Think of this as the gold standard for transparency. It breaks down the costs, showing you the non-negotiable wholesale rates (interchange and assessments) and, separately, what your provider is charging on top. You see their exact markup.

If a provider tries to steer you toward a Tiered or Flat-Rate model without a compelling reason, that's a major red flag. These models often hide the real costs and can cause you to overpay on simple, low-risk transactions, like when a customer uses a debit card.

Read Every Word of the Contract

Before you sign on the dotted line, you have to read the fine print. It’s tedious, but it’s essential. Many processors use long-term contracts—sometimes for three years or more—to lock you in. If you try to leave before the term is up, they’ll slap you with a hefty Early Termination Fee (ETF).

Your best bet is to look for providers offering month-to-month agreements. This keeps them honest and motivated to deliver great service, because you have the freedom to walk away without a penalty. Also, keep an eye out for any auto-renewal clauses that can make switching a nightmare.

Choosing a payment processor is more than just a transaction; it's a partnership. Your provider should feel like an extension of your team, offering clear communication, reliable support, and a fee structure that helps your business thrive, not just survive.

High fees are a massive headache for businesses everywhere. A recent merchant survey revealed that 72% of businesses view high transaction fees as a major challenge that directly eats into their cash flow and profit margins. With total card fees in the U.S. ballooning to an estimated $236 billion recently, the financial weight of these costs is impossible to ignore. Discover more insights about the challenges merchants face on The Payments Association website.

Ask the Tough Questions and Test Their Support

When you're comparing providers, show up prepared with a list of direct questions. How they answer will tell you everything you need to know about their transparency and business practices.

Here’s a checklist to get you started:

- Pricing Model: "Can you give me a full, detailed Interchange-Plus quote? What is your exact markup?"

- All Fees: "Please provide a complete schedule of every single fee I could be charged. I want to see monthly fees, annual fees, PCI compliance fees, and any chargeback fees."

- Contract Terms: "Is this a month-to-month agreement? Are there any early termination penalties?"

- Customer Support: "What are your support hours? If I have a problem, will I be talking to a real person or a bot? Do I get a dedicated contact?"

- Hardware and Software: "Is your POS equipment proprietary? If I decide to switch providers, can I still use this hardware, or will I be forced to buy new gear?"

Arming yourself with this information helps you cut through the marketing fluff and choose a payment processor that actually works for your business and your bottom line.

Your Top Questions About Merchant Fees, Answered

If you're scratching your head about merchant fees, you're not alone. It's a complex part of running a business, but understanding it is key. Here are some straightforward answers to the questions we hear most often.

Can I Just Avoid Merchant Fees Altogether?

The short answer is no, not if you want to accept credit or debit cards. These fees are a built-in cost of the convenience and security that card payments offer.

Of course, you could always go cash-only, but in a world where customers expect to tap and pay, you'd likely lose more in sales than you'd save in fees. The real goal isn't to eliminate fees but to minimize them with the right pricing model and smart business practices.

Why Do Online Sales Cost More to Process?

It all boils down to a single word: risk. When a customer buys something online, it's called a 'Card-Not-Present' (CNP) transaction. Because you can't physically see the card or the customer, the chances of fraud are significantly higher.

To cover this increased risk, the card networks (like Visa and Mastercard) set higher interchange rates for online sales. They're essentially charging a little extra to protect the bank that issued the card from potential losses.

What's the Difference Between a Merchant Account and a Payment Processor?

This one trips up a lot of people, but a simple analogy helps.

Think of your merchant account as a dedicated holding pen for your money. It's a special bank account where funds from card sales are temporarily held before they get moved into your main business bank account.

The payment processor is the technology partner that makes the whole transaction happen. They're the ones connecting your terminal or website to the card networks and banks, ensuring the data is transmitted securely. Today, many providers bundle these two services together into one neat package.

How Often Should I Actually Look at My Statements?

You should make a habit of reviewing your merchant statement every single month. A quick scan can help you catch new or hidden fees, sudden rate increases, or simple billing mistakes before they turn into a real problem.

Beyond that, it's smart to do a deeper dive at least once a year. This is your chance to see how your current rates stack up against the competition and make sure you're still getting a fair deal.

Ready to take control of your payment processing with a system designed for clarity and savings? Biyo POS offers an all-in-one solution that integrates payments, inventory, and customer management seamlessly. Explore our features and see how you can streamline operations by visiting https://biyopos.com.